Exhibit 99.1

InfuSystem Holdings, Inc. Sidoti& Company LLC Conference January 13, 2014 Eric K. Steen, CEO Jonathan P. Foster, CFO

Safe Harbor Statement Certain statements contained in this presentation are forward -looking statements and are based on future expectations, plans and prospects for InfuSystem Holdings, Inc.’s (“InfuSystem”, “INFU”, “the Company”, “We”) business and operations that involve a number of risks and uncertainties. InfuSystem’s outlook for 2014-2015 and other forward -looking statements in this release are made as of January 13, 2014, and the Company disclaims any duty to supplement, update or revise such statements on a going-forward basis, whether as a result of subsequent developments, changed expectations or otherwise. In connection with the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995, the Company is identifying certain factors that could cause actual results to differ, perhaps materially, from those indicated by these forward -looking statements. Those factors, risks and uncertainties include, but are not limited to, potential changes in overall healthcare reimbursement – including CMS competitive bidding, sequestration, concentration of customers, increased focusonearly detection ofcancer, competitive treatments, dependency on Medicare Supplier Number, availability of chemotherapy drugs, global financial conditions, changes and enforcement of state and federal laws,naturalforces, competition, dependency on suppliers, risksin acquisitions &joint ventures, US Healthcare Reform, relationships with healthcare professionals and organizations, technological changes related to infusion therapy, dependency on websites and intellectual property, the ability of the Company to successfully integrate acquired businesses, dependency on key personnel, dependency on banking relations and covenants, and other risks associated with our common stock, as well as any other litigation to which the Company may be subject from time to time; and other risk factors as discussed in the Company’s annual report on Form 10-K for the year ended December 31, 2012 and in other filings, including Forms 10-Q, made by the Company fromtimetotimewiththe Securities and Exchange Commission.

InfuSystem at a Glance Company Overview Innovative provider and supplier of infusion services Market leader in oncology home infusion with 40,000 patients a year –25 Year business model World-class pump rentals and service to providers, manufacturers, and (1) other rental companies in the US and Canada 46,000 InfuSystem pump fleet generating revenue from both payors and providers 2013 9-Month Financials Revenues $45.1M (Up 6%) AEBITDA $11.3M (Up 8%) Free Cash Flow $9.2M (Up 73%) Market Cap $37.65M @ $1.72

Full Line Multi-Therapy & Multi-Point Offering Payor Patient Partne Provider Device & Pharma Manufacturer, Distributor, GPO, ACO

Positioned For Growth Market Trends • InfuSystem is uniquely positioned to take advantage of market trends Leadership •Leadership can now focus on running a business for first time in over a year Strategy •Transformational strategy is developed and being implemented

InfuSystem Niche – Extension of Clinic to Home Ambulatory Home Infusion 25-year old business model in DME billing At home, at work, at play, all while receiving the drug High satisfaction scores 24/7 on-call oncology nurses Proven outcomes with continuous home infusion Oncology, Post Surgical Pain, Special Disease States TPP Payor Contracts Bills patient insurance 250+ Commercial and Government Payor Contracts Commercial Payors reimburse more therapies than CMS Awarded contracts in all 9MSAs (1 of 3 National Vendors) Average cuts of ~21% for our category, per CMS ($250,000 per yr)

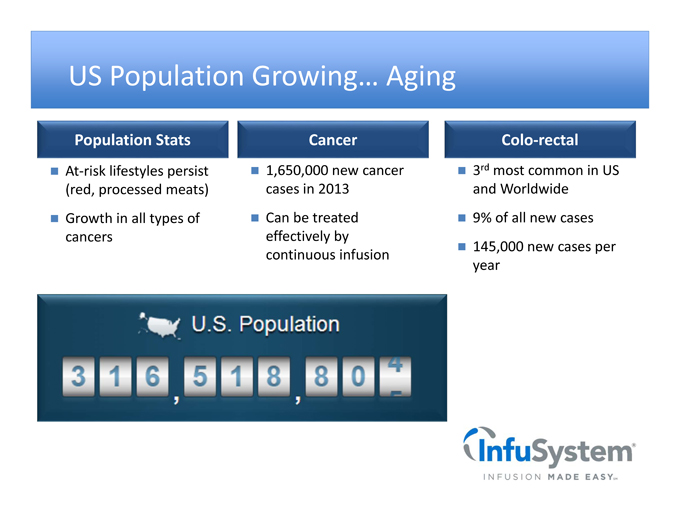

US Population Growing … Aging Population Stats At-risk lifestyles persist (red, processed meats) Growth in all types of cancers Cancer 1,650,000 new cancer cases in 2013 Can be treated effectively by continuous infusion Colo-rectal 3rd most common in US and Worldwide 9% of all new cases 145,000 new cases per year

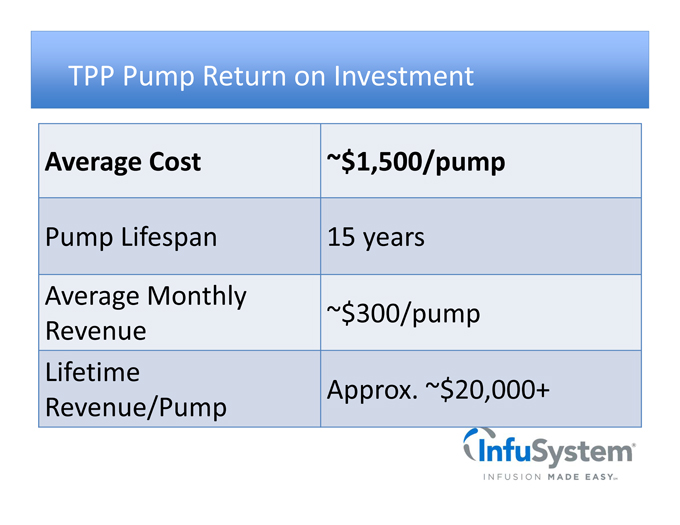

TPP Pump Return on Investment Average Cost ~$1,500/pump Pump Lifespan 15years Average Monthly ~$300/pump Revenue Lifetime Approx. ~$20,000+ Revenue/Pump

Increasing Therapy Offerings to Payors Oncology Payor Infectious Disease Surgery Special Disease States

Rentals, Sales & Service to Providers Pump Rentals, Sales and Asset Management Pump Experts Direct sales, rental, and lease of device and supplies in US and Canada Pump Broker Expertise –ability to acquire and dispose of CAP EX in cost effective way Asset management, rental and lease Preventative Maint. Annual Pump Recertification Preventative Maintenance Warranty Repair World-Class ISO Certified service facilities Regional Distribution West, South, East & Canada 28 Certified Technicians

Offering Infusion to All Points of Care Home Infusion Provider Long Term Care Emergency Services Oncology Acute Care

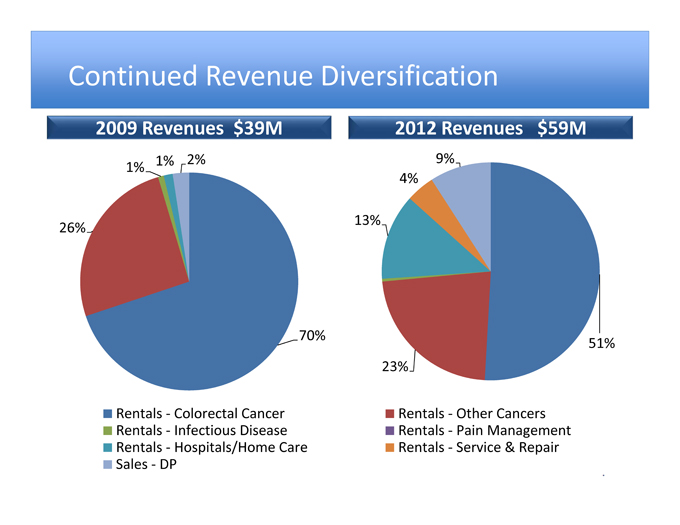

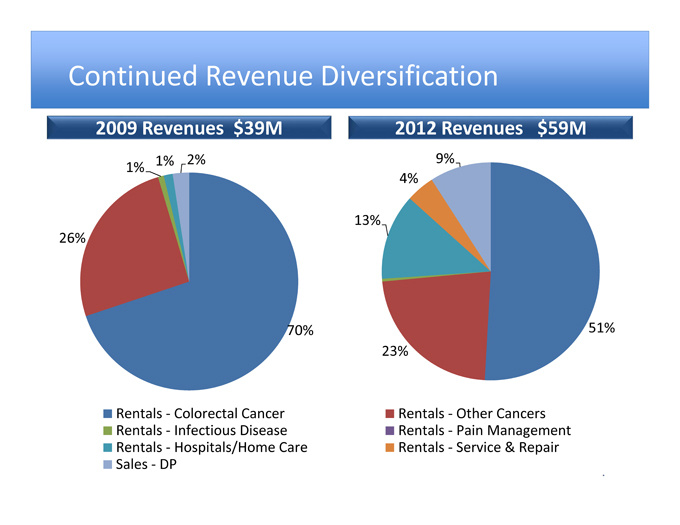

Continued Revenue Diversification 2009 Revenues $39M 1% 1% 2% 26% 70% Rentals - Colorectal Cancer Rentals - Infectious Disease Rentals - Hospitals/Home Care Sales - DP 2012 Revenues $59M 9% 4% 13% 51% 23% Rentals - Other Cancers Rentals -Pain Management Rentals - Service & Repair

Connectivity through EMR , Web Portal and System Interface

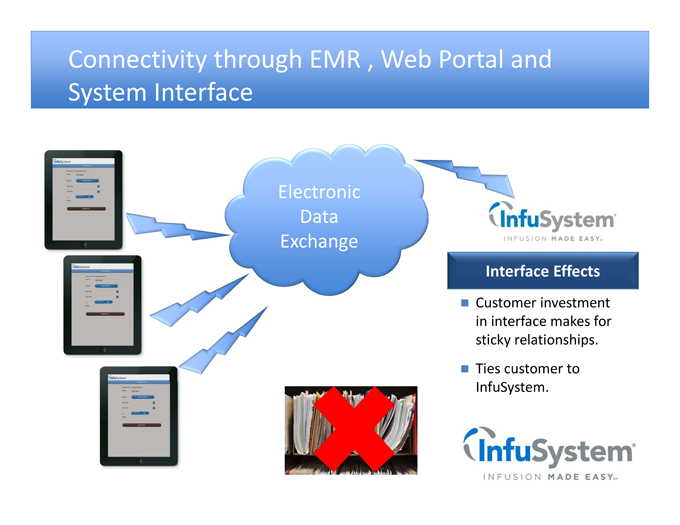

Connectivity through EMR , Web Portal and System Interface Electronic Data Exchange Interface Effects Customer investment in interface makes for sticky relationships. Ties customer to InfuSystem.

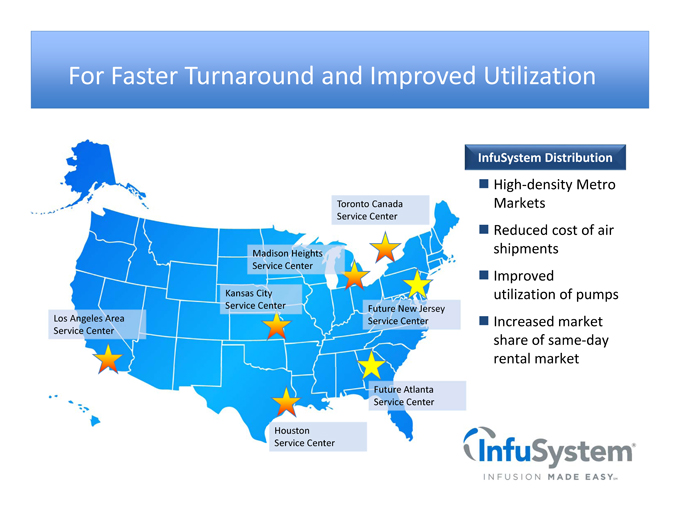

For Faster Turnaround and Improved Utilization InfuSystem Distribution High-density Metro Markets Reduced cost of air shipments Improved utilization of pumps Increased market share of same-day rental market

Where Does This Get INFU In Three Years ? Aging Population and Cancer Growth More Patients Home IV , Commercial Pay Recognizing Value, CMS Competitive Bidding Peripheral Nerve Block and Smart Pump Growth Revenue Growth in High Single Digits Through 2015

Financial Review

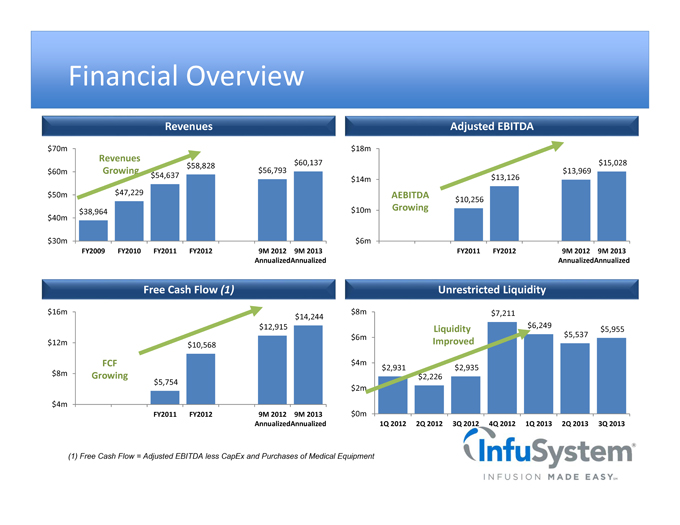

Financial Overview Revenues $70m Revenues $58,828 $60,137 $60m Growing $56,793 $54,637 $50m $47,229 $40m $38,964 $30m FY2009 FY2010 FY2011 FY2012 9M 2012 9M 2013 Annualized Annualized Free Cash Flow (1) $16m $14,244 $12,915 $12m $10,568 FCF $8m Growing $5,754 $4m FY2011 FY2012 9M 2012 9M 2013 Annualized Annualized Adjusted EBITDA $18m $15,028 $13,126 $13,969 $14m AEBITDA $10,256 $10m Growing $6m FY2011 FY2012 9M 2012 9M 2013 Annualized Annualized Unrestricted Liquidity $8m $7,211 $6,249 Liquidity $5,955 $6m $5,537 Improved $4m $2,931 $2,935 $2,226 $2m $0m 1Q 2012 2Q 2012 3Q 2012 4Q 2012 1Q 2013 2Q 2013 3Q 2013 (1) Free Cash Flow = Adjusted EBITDA less CapEx and Purchases of Medical Equipment

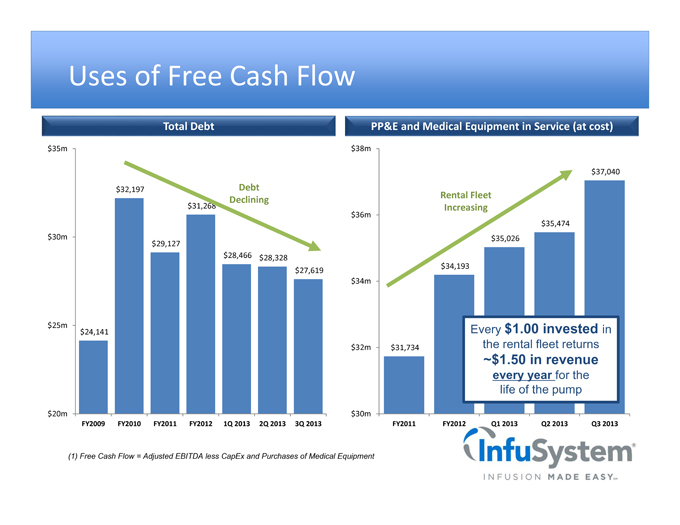

Uses of Free Cash Flow Total Debt $35m $32,197 Debt Declining $31,268 $30m $29,127 $28,466 $28,328 $27,619 $25m $24,141 $20m FY2009 FY2010 FY2011 FY2012 1Q 2013 2Q 2013 3Q 2013 PP&E and Medical Equipment in Service (at cost) $38m $37,040 Rental Fleet $36m Increasing $35,474 $35,026 $34,193 $34m Every $1.00 invested in $32m $31,734 the rental fleet returns ~$1.50 in revenue every year for the life of the pump $30m FY2011 FY2012 Q1 2013 Q2 2013 Q3 2013 (1) Free Cash Flow = Adjusted EBITDA less CapEx and Purchases of Medical Equipment

Take Away

Positioned For Growth Market Trends • InfuSystem is uniquely positioned to take advantage of market trends Leadership •Leadership can now focus on running a business for first time in over a year Strategy •Transformational strategy is developed and being implemented

Thank You for Your Interest! IR Contact Info: The Dilenschneider Group 212-922-0900 Rob Swadosh, rswadosh@dgi-nyc.com Patrick Malone, pmalone@dgi-nyc.com

Appendix: INFU Overview

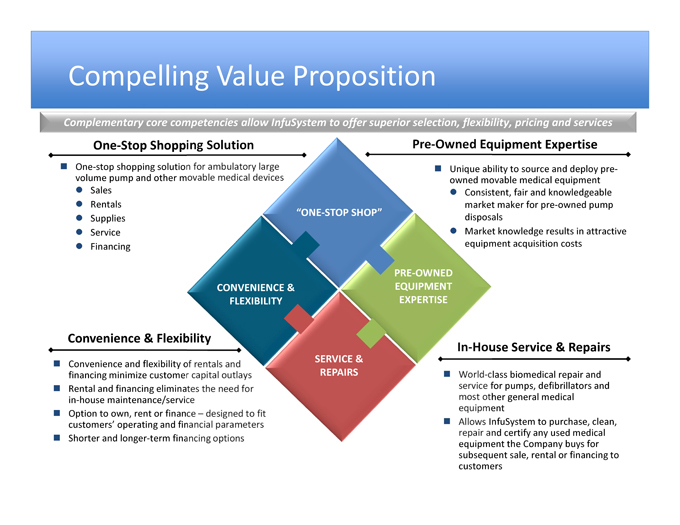

Compelling Value Proposition Complementary core competencies allow InfuSystem to offer superior selection, flexibility, pricing and services One-Stop Shopping - One-stop shopping solution volume pump and other Sales Rentals Supplies Service Financing Convenience & Flex Convenience and flexibility financing minimize customer Rental and financing eliminates in-house maintenance/service Option to own, rent or finance customers’ operating and Shorter and longer-term quipment Expertise Unique ability to source and deploy pre-owned movable medical equipment Consistent, fair and knowledgeable market maker for pre-owned pump disposals Market knowledge results in attractive equipment acquisition costs Service & Repairs class biomedical repair and for pumps, defibrillators and other general medical InfuSystem to purchase, clean, and certify any used medical equipment the Company buys for subsequent sale, rental or financing to customers

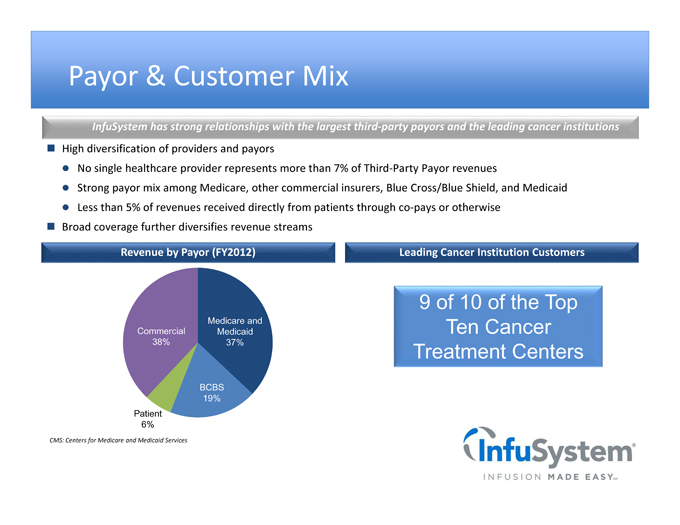

Payor & Customer Mix InfuSystem has strong relationships with the largest third-party payorsand the leading cancer institutions High diversification of providers and payors No single healthcare provider represents more than 7% of Third-Party Payor revenues Strong payor mix among Medicare, other commercial insurers, Blue Cross/Blue Shield, and Medicaid Less than 5% of revenues received directly from patients through co pays or otherwise Broad coverage further diversifies revenue streams Revenue by Payor (FY2012) Medicare and Commercial Medicaid 38% 37% BCBS 19% Patient 6% Leading Cancer Institution Customers 9 of 10 of the Top Ten Cancer Treatment Centers CMS: Centers for Medicare and Medicaid Services

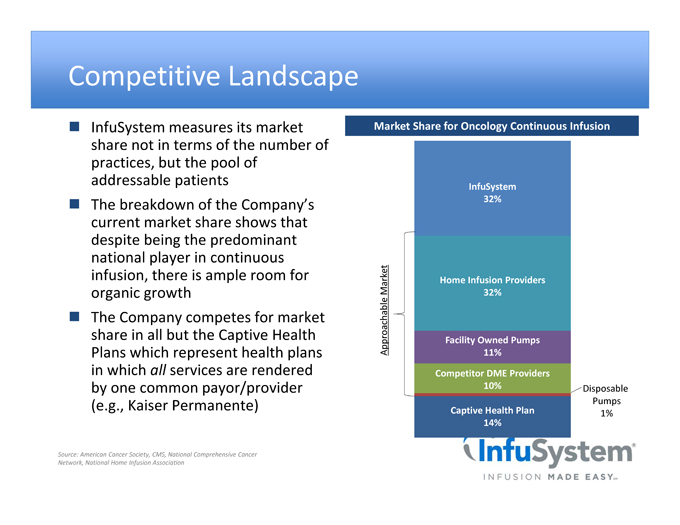

Competitive Landscape InfuSystem measures its market share not in terms of the number of practices, but the pool of addressable patients The breakdown of the Company’s current market share shows that despite being the predominant national player in continuous infusion, there is ample room for organic growth The Company competes for market share in all but the Captive Health Plans which represent health plans in which all services are rendered by one common payor/provider (e.g., Kaiser Permanente) Market Share for Oncology Continuous Infusion InfuSystem 32% Market Home Infusion Providers 32% Facility Owned Pumps Approachable 11% Competitor DME Providers 10% Disposable Pumps Captive Health Plan 1% 14% Source: American Cancer Society, CMS, National Comprehensive Cancer Network, National Home Infusion Association

Direct Payor Business Model InfuSystem’s Direct Payor business is focused primarily on the sale, rental, financing and accompanying service of movable medical equipment to hospitals and alternate care sites who pay InfuSystem directly –no third-party reimbursement Founded in 1998 and headquartered in Olathe, KS with distribution/service centers in Santa Fe Springs, CA and Mississauga, Ontario InfuSystem services –ISO 9001 and repairs movable medical equipment Leading provider to alternate site healthcare facilities and hospitals in the United States and Canada Home infusion providers, long-term care, physician clinics, research facilities, etc. Transacts directly with healthcare providers –no third-party reimbursement revenue Products InfuSystem sells, rents and finances a wide variety of new and used large volume and ambulatory pumps Infusion pumps Syringe pumps Enteral pumps Ambulatory pumps Service & Repair InfuSystem services and repairs both its own fleet of pumps and many types of other movable medical equipment Large volume pumps Fluid collection Ambulatory pumps Medical equipment

Direct Payor Offerings Leading Provider of New and Pre-Owned Pumps InfuSystem offers new pumps from top brands Broker-dealer trading desk In addition, over 70 models and versions of pre-owned pumps are offered Pre-owned pumps are re-built and certified by in-house biomedical technicians to be patient ready Warranty offered on pre-owned pumps A variety of financing options to fit customers’ operating, budgeting and financing parameters Nationwide, industry leading ISO 9001 service programs Launching branch service center in Houston Pre-Owned & New Pumps from Top Manufacturers Full Spectrum of Ownership Options for Customers Rental Sales Asset Management Renting new or pre-owned equipment Industry leader in sales of pre-owned ISO 9001 Service offered equipment, creating significant savings Service plans offered Rent pumps by the day, week or month Local service expansion to match swings in patient count Competitive pricing on new equipment 2 existing; 1 planned Free shipping on all rentals Option to sell back pre-owned pumps Coordinate with TPP Loaner pumps available Leasing plans offered

Medical Equipment Service & Repair In addition to supporting and repairing InfuSystem’s in-house fleet, the Company certifies, recalibrates, repairs and services a variety of infusion pumps Pumps require scheduled maintenance and calibration in accordance with manufacturer’s specifications and regulatory guidelines Service and repair capabilities on high demand services reaching end of life that are no longer supported by manufacturers ISO certification and an established quality system strengthens relationships with major customers Provides InfuSystem an opportunity to establish a business relationship with customers that acquired pumps through other sources Continuing and increased need for compliance with current as well as anticipated regulations 28 highly qualified service technicians 5major manufacturer relationships: 3service centers, located in California, Toronto and Kansas

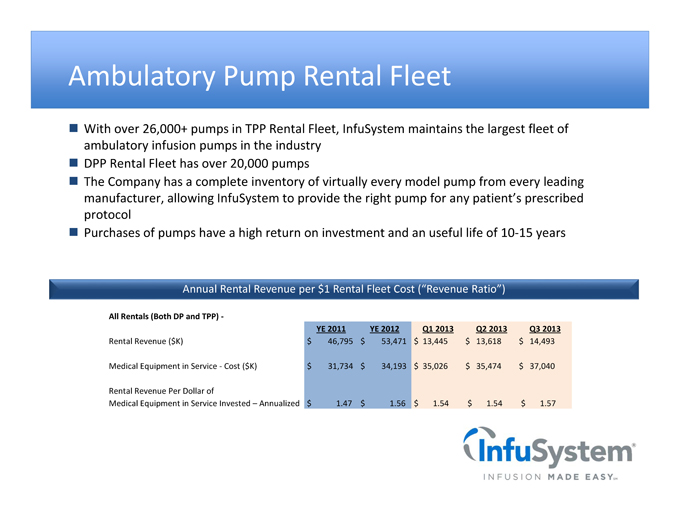

Ambulatory Pump Rental Fleet With over 26,000+ pumps in TPP Rental Fleet, InfuSystem maintains the largest fleet of ambulatory infusion pumps in the industry DPP Rental Fleet has over 20,000 pumps The Company has a complete inventory of virtually every model pump from every leading manufacturer, allowing InfuSystem to provide the right pump for any patient’s prescribed protocol Purchases of pumps have a high return on investment and an useful life of 10 15 years Annual Rental Revenue per $1 Rental Fleet Cost (“Revenue Ratio”) All Rentals (Both DP and TPP) YE 2011 YE 2012 Q1 2013 Q2 2013 Q3 2013 Rental Revenue ($K) $ 46,795 $ 53,471 $ 13,445 $ 13,618 $ 14,493 Medical Equipment in Service Cost ($K) $ 31,734 $ 34,193 $ 35,026 $ 35,474 $ 37,040 Rental Revenue Per Dollar of Medical Equipment in ServiceInvested –Annualized $ 1.47 $ 1.56 $ 1.54 $ 1.54 $ 1.57

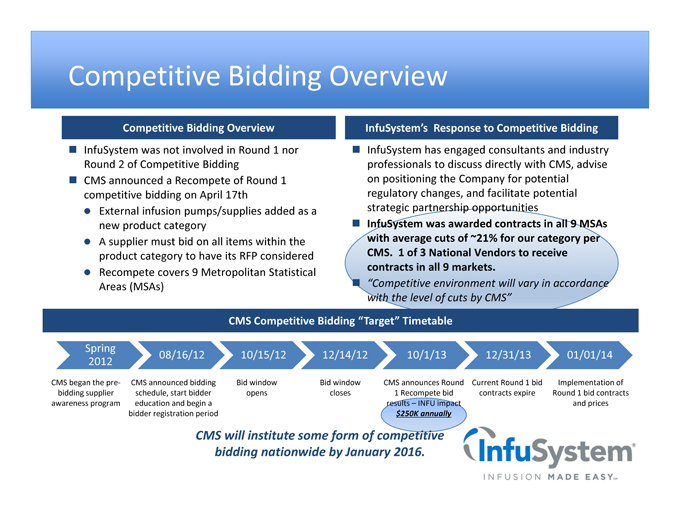

Competitive Bidding Overview Competitive Bidding Overview InfuSystem was not involved in Round 1 nor Round 2 of Competitive Bidding CMS announced a Recompete of Round 1 competitive bidding on April 17th External infusion pumps/supplies added as a new product category A supplier must bid on all items within the product category to have its RFP considered Recompete covers 9 Metropolitan Statistical Areas (MSAs) InfuSystem’s Response to Competitive Bidding InfuSystem has engaged consultants and industry professionals to discuss directly with CMS, advise on positioning the Company for potential regulatory changes, and facilitate potential strategic partnership opportunities InfuSystem was awarded contracts in all 9 MSAs with average cuts of ~21% for our category per CMS. 1 of 3 National Vendors to receive contracts in all 9 markets. “Competitive environment will vary in accordance with the level of cuts by CMS” CMS Competitive Bidding “Target” Timetable Spring 08/16/12 10/15/12 12/14/12 10/1/13 12/31/13 01/01/14 2012 CMS began the pre CMS announced bidding Bid window Bid window CMS announces Round Current Round 1 bid Implementation of bidding supplier schedule, start bidder opens closes 1 Recompete bid contracts expire Round 1 bid contracts awareness program education and begin a results –INFU impact and prices bidder registration period $250K annually CMS will institute some form of competitive bidding nationwide by January 2016.

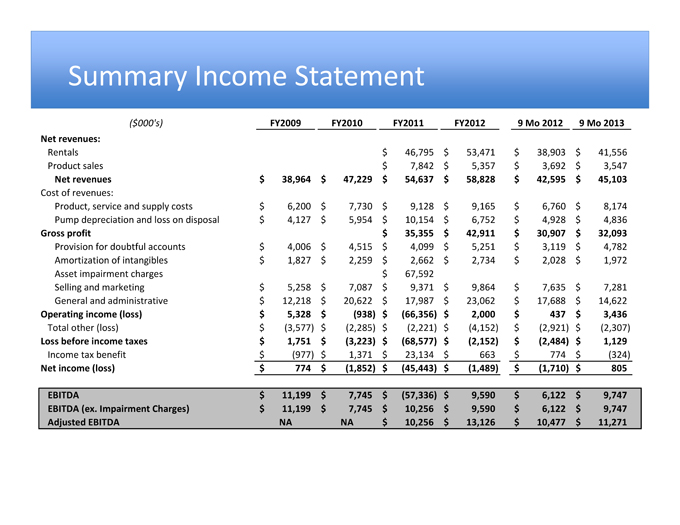

Summary Income Statement ($000’s) FY2009 FY2010 FY2011 FY2012 9 Mo 2012 9 Mo 2013 Net revenues: Rentals $ 46,795 $ 53,471 $ 38,903 $ 41,556 Product sales $ 7,842 $ 5,357 $ 3,692 $ 3,547 Net revenues $ 38,964 $ 47,229 $ 54,637 $ 58,828 $ 42,595 $ 45,103 Cost of revenues: Product, service and supply costs $ 6,200 $ 7,730 $ 9,128 $ 9,165 $ 6,760 $ 8,174 Pump depreciation and loss on disposal $ 4,127 $ 5,954 $ 10,154 $ 6,752 $ 4,928 $ 4,836 Gross profit $ 35,355 $ 42,911 $ 30,907 $ 32,093 Provision for doubtful accounts $ 4,006 $ 4,515 $ 4,099 $ 5,251 $ 3,119 $ 4,782 Amortization of intangibles $ 1,827 $ 2,259 $ 2,662 $ 2,734 $ 2,028 $ 1,972 Asset impairment charges $ 67,592 Selling and marketing $ 5,258 $ 7,087 $ 9,371 $ 9,864 $ 7,635 $ 7,281 General and administrative $ 12,218 $ 20,622 $ 17,987 $ 23,062 $ 17,688 $ 14,622 Operating income (loss) $ 5,328 $ (938) $ (66,356) $ 2,000 $ 437 $ 3,436 Total other (loss) $ (3,577) $ (2,285) $ (2,221) $ (4,152) $ (2,921) $ (2,307) Loss before income taxes $ 1,751 $ (3,223) $ (68,577) $ (2,152) $ (2,484) $ 1,129 Income tax benefit $ (977) $ 1,371 $ 23,134 $ 663 $ 774 $ (324) Net income (loss) $ 774 $ (1,852) $ (45,443) $ (1,489) $ (1,710) $ 805 EBITDA $ 11,199 $ 7,745 $ (57,336) $ 9,590 $ 6,122 $ 9,747 EBITDA (ex. Impairment Charges) $ 11,199 $ 7,745 $ 10,256 $ 9,590 $ 6,122 $ 9,747 Adjusted EBITDA NA NA $ 10,256 $ 13,126 $ 10,477 $ 11,271

Continued Revenue Diversification 2009 Revenue 1% 1% 2% 26% 70% Rentals - Colorectal Cancer Rentals - Infectious Disease Rentals - Hospitals/Home Care Sales - DP Rentals - Other Cancers Rentals - Pain Management Rentals - Service & Repair

Continued Revenue Diversification 2009 Revenues $39M 1% 1% 2% 26% 70% Rentals - Colorectal Cancer Rentals - Infectious Disease Rentals - Hospitals/Home Care Sales - DP 2012 Revenues $59M 9% 4% 13% 51% 23% Rentals - Other Cancers Rentals -Pain Management Rentals - Service & Repair

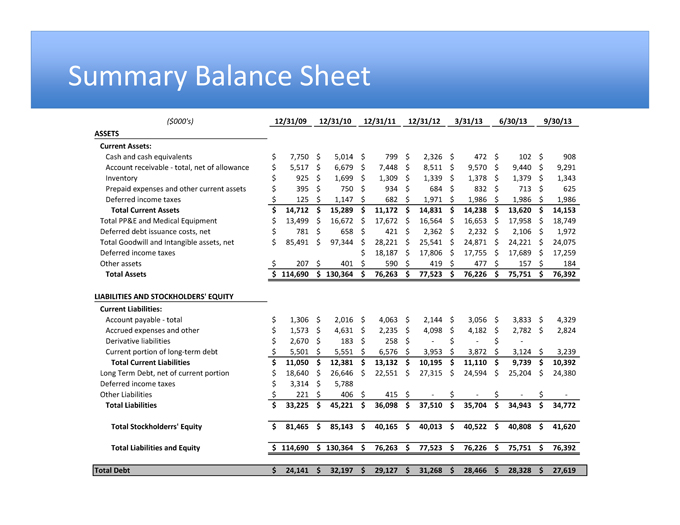

Summary Balance Sheet ($000’s) 12/31/09 12/31/10 12/31/11 12/31/12 3/31/13 6/30/13 9/30/13 ASSETS Current Assets: Cash and cash equivalents $ 7,750 $ 5,014 $ 799 $ 2,326 $ 472 $ 102 $ 908 Account receivable - total, net of allowance $ 5,517 $ 6,679 $ 7,448 $ 8,511 $ 9,570 $ 9,440 $ 9,291 Inventory $ 925 $ 1,699 $ 1,309 $ 1,339 $ 1,378 $ 1,379 $ 1,343 Prepaid expenses and other current assets $ 395 $ 750 $ 934 $ 684 $ 832 $ 713 $ 625 Deferred income taxes $ 125 $ 1,147 $ 682 $ 1,971 $ 1,986 $ 1,986 $ 1,986 Total Current Assets $ 14,712 $ 15,289 $ 11,172 $ 14,831 $ 14,238 $ 13,620 $ 14,153 Total PP&E and Medical Equipment $ 13,499 $ 16,672 $ 17,672 $ 16,564 $ 16,653 $ 17,958 $ 18,749 Deferred debt issuance costs, net $ 781 $ 658 $ 421 $ 2,362 $ 2,232 $ 2,106 $ 1,972 Total Goodwill and Intangible assets, net $ 85,491 $ 97,344 $ 28,221 $ 25,541 $ 24,871 $ 24,221 $ 24,075 Deferred income taxes $ 18,187 $ 17,806 $ 17,755 $ 17,689 $ 17,259 Other assets $ 207 $ 401 $ 590 $ 419 $ 477 $ 157 $ 184 Total Assets $ 114,690 $ 130,364 $ 76,263 $ 77,523 $ 76,226 $ 75,751 $ 76,392 LIABILITIES AND STOCKHOLDERS’ EQUITY Current Liabilities: Account payable - total $ 1,306 $ 2,016 $ 4,063 $ 2,144 $ 3,056 $ 3,833 $ 4,329 Accrued expenses and other $ 1,573 $ 4,631 $ 2,235 $ 4,098 $ 4,182 $ 2,782 $ 2,824 Derivative liabilities $ 2,670 $ 183 $ 258 $ - $ - $ - Current portion of long-term debt $ 5,501 $ 5,551 $ 6,576 $ 3,953 $ 3,872 $ 3,124 $ 3,239 Total Current Liabilities $ 11,050 $ 12,381 $ 13,132 $ 10,195 $ 11,110 $ 9,739 $ 10,392 Long Term Debt, net of current portion $ 18,640 $ 26,646 $ 22,551 $ 27,315 $ 24,594 $ 25,204 $ 24,380 Deferred income taxes $ 3,314 $ 5,788 Other Liabilities $ 221 $ 406 $ 415 $ - $ - $ - $ - Total Liabilities $ 33,225 $ 45,221 $ 36,098 $ 37,510 $ 35,704 $ 34,943 $ 34,772 Total Stockholderrs’ Equity $ 81,465 $ 85,143 $ 40,165 $ 40,013 $ 40,522 $ 40,808 $ 41,620 Total Liabilities and Equity $ 114,690 $ 130,364 $ 76,263 $ 77,523 $ 76,226 $ 75,751 $ 76,392 Total Debt $ 24,141 $ 32,197 $ 29,127 $ 31,268 $ 28,466 $ 28,328 $ 27,619

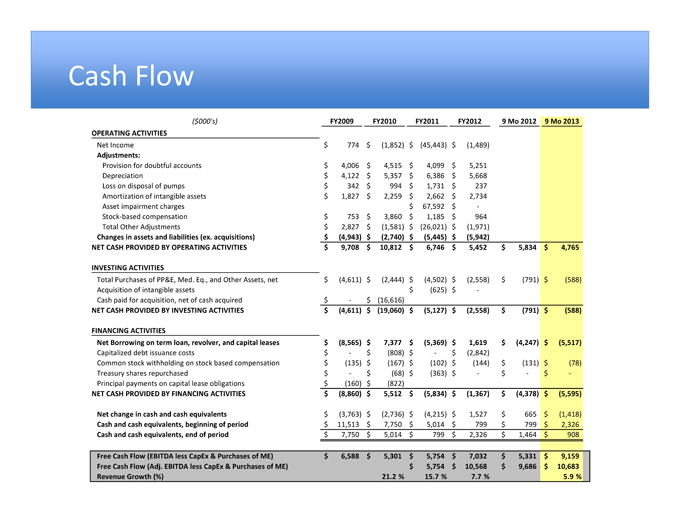

Cash Flow ($000’s) FY2009 FY2010 FY2011 FY2012 9 Mo 2012 9 Mo 2013 OPERATING ACTIVITIES Net Income $ 774 $ (1,852) $ (45,443) $ (1,489) Adjustments: Provision for doubtful accounts $ 4,006 $ 4,515 $ 4,099 $ 5,251 Depreciation $ 4,122 $ 5,357 $ 6,386 $ 5,668 Loss on disposal of pumps $ 342 $ 994 $ 1,731 $ 237 Amortization of intangible assets $ 1,827 $ 2,259 $ 2,662 $ 2,734 Asset impairment charges $ 67,592 $ -Stock-based compensation $ 753 $ 3,860 $ 1,185 $ 964 Total Other Adjustments $ 2,827 $ (1,581) $ (26,021) $ (1,971) Changes in assets and liabilities (ex. acquisitions) $ (4,943) $ (2,740) $ (5,445) $ (5,942) NET CASH PROVIDED BY OPERATING ACTIVITIES $ 9,708 $ 10,812 $ 6,746 $ 5,452 $ 5,834 $ 4,765 INVESTING ACTIVITIES Total Purchases of PP&E, Med. Eq., and Other Assets, net $ (4,611) $ (2,444) $ (4,502) $ (2,558) $ (791) $ (588) Acquisition of intangible assets $ (625) $ -Cash paid for acquisition, net of cash acquired $ - $ (16,616) NET CASH PROVIDED BY INVESTING ACTIVITIES $ (4,611) $ (19,060) $ (5,127) $ (2,558) $ (791) $ (588) FINANCING ACTIVITIES Net Borrowing on term loan, revolver, and capital leases $ (8,565) $ 7,377 $ (5,369) $ 1,619 $ (4,247) $ (5,517) Capitalized debt issuance costs $ - $ (808) $ - $ (2,842) Common stock withholding on stock based compensation $ (135) $ (167) $ (102) $ (144) $ (131) $ (78) Treasury shares repurchased $ - $ (68) $ (363) $ - $ - $ - Principal payments on capital lease obligations $ (160) $ (822) NET CASH PROVIDED BY FINANCING ACTIVITIES $ (8,860) $ 5,512 $ (5,834) $ (1,367) $ (4,378) $ (5,595) Net change in cash and cash equivalents $ (3,763) $ (2,736) $ (4,215) $ 1,527 $ 665 $ (1,418) Cash and cash equivalents, beginning of period $ 11,513 $ 7,750 $ 5,014 $ 799 $ 799 $ 2,326 Cash and cash equivalents, end of period $ 7,750 $ 5,014 $ 799 $ 2,326 $ 1,464 $ 908 Free Cash Flow (EBITDA less CapEx & Purchases of ME) $ 6,588 $ 5,301 $ 5,754 $ 7,032 $ 5,331 $ 9,159 Free Cash Flow (Adj. EBITDA less CapEx & Purchases of ME) $ 5,754 $ 10,568 $ 9,686 $ 10,683 Revenue Growth (%) 21.2 % 15.7 % 7.7 % 5.9 %