UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C., 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 000-51902

INFUSYSTEM HOLDINGS, INC.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 20-3341405 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

31700 Research Park Drive

Madison Heights, Michigan 48071

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code:

(248) 291-1210

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Exchange on which Registered | |

| Common Stock, par value $0.0001 per share | New York Stock Exchange Amex |

Securities Registered Pursuant to Section 12(g) of the Act:

None

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter periods as the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES ¨ NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (check one)

| Large accelerated filer | ¨ | Accelerated filer ¨ | ||

| Non-accelerated filer | ¨ | Smaller reporting company x | ||

| (Do not check if smaller reporting company.) | ||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ¨ NO x

The aggregate market value of the registrant’s voting equity held by non-affiliates of the registrant, computed by reference to the closing sales price for the registrant’s common stock on June 30, 2010, as reported on the OTC Bulletin Board, was approximately $40,828,912. In determining the market value of the voting equity held by non-affiliates, securities of the registrant beneficially owned by directors and officers of the registrant have been excluded. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares of the registrant’s common stock outstanding as of March 9, 2011 was 21,105,506.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of this registrant’s definitive proxy statement for its 2011 Annual Meeting of Stockholders to be filed with the SEC no later than 120 days after the end of the registrant’s fiscal year are incorporated herein by reference in Part III of this Annual Report on Form 10-K.

Cautionary Statement about Forward-Looking Statements

This Annual Report on Form 10-K includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements other than statements of historical facts contained in this Annual Report on Form 10-K, including statements regarding the future financial position, business strategy, plans, and objectives of management for future operations, are forward-looking statements. The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “expect,” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on current expectations and projections about future events and financial trends that we believe may affect financial condition, results of operations, business strategy and financial needs. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including, without limitation, those described in “Risk Factors” and elsewhere in this Annual Report on Form 10-K, including, among other things:

| • | dependence on our Medicare Supplier Number; |

| • | changes in third-party reimbursement rates; |

| • | availability of chemotherapy drugs used in our infusion pump systems; |

| • | physician’s acceptance of infusion pump therapy over oral medications; |

| • | our growth strategy, involving entry into new fields of infusion-based therapy; |

| • | the current global financial crisis; |

| • | industry competition; and |

| • | dependence upon our suppliers. |

These risks are not exhaustive. Other sections of this Annual Report on Form 10-K include additional factors which could adversely impact our business and financial performance. Moreover, we operate in a very competitive and rapidly changing environment. New risk factors emerge from time to time and it is not possible for us to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

You should not rely upon forward looking statements as predictions of future events. We cannot assure you that the events and circumstances reflected in the forward looking statements will be achieved or occur. Although we believe that the expectations reflected in the forward looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements.

1

References in this Annual Report on Form 10-K to “we,” “us,” or the “Company” are to InfuSystem Holdings, Inc. and its subsidiaries.

| Item 1. | Business. |

Background

We were formed as a Delaware blank check company in 2005 for the purpose of acquiring through a merger, capital stock exchange, asset acquisition or other similar business combination, one or more operating businesses in the healthcare sector. We completed our initial public offering on April 18, 2006. On September 29, 2006, we entered into a Stock Purchase Agreement (as, amended the “Stock Purchase Agreement”) with I-Flow Corporation (I-Flow), Iceland Acquisition subsidiaries, our wholly-owned subsidiaries, and InfuSystem, a wholly-owned subsidiary of I-Flow Corporation. Upon the closing of the transactions contemplated by the Stock Purchase Agreement on October 25, 2007, Iceland Acquisition subsidiaries purchased all of the issued and outstanding capital stock of InfuSystem from I-Flow and concurrently merged with and into InfuSystem. As a result of the merger, Iceland Acquisition subsidiaries ceased to exist as an independent entity and InfuSystem, as the corporation surviving the merger, became our wholly-owned subsidiary Effective October 25, 2007, we changed our corporate name from HAPC, INC. to InfuSystem Holdings, Inc.

InfuSystem was incorporated under the laws of the State of California in December 1997 under the name I-Flow subsidiary, Inc., as a wholly owned subsidiary of I-Flow. In February 1998, I-Flow subsidiary, Inc. acquired Venture Medical, Inc. and InfuSystem II, Inc. in a merger transaction pursuant to which I-Flow subsidiary, Inc. as the surviving corporation changed its name to InfuSystem, Inc.

Business Concept and Strategy

The Company is the leading provider of infusion pumps and related services. The Company services hospitals, oncology practices and other alternate site healthcare providers. Headquartered in Madison Heights, Michigan, the Company delivers local, field-based customer support, and also operates pump service and repair Centers of Excellence in Michigan, Kansas, California, and Ontario, Canada.

Our core service is to supply electronic ambulatory infusion pumps and associated disposable supply kits to oncology practices, infusion clinics and hospital outpatient chemotherapy clinics to be utilized in the treatment of a variety of cancers including colorectal cancer. Colorectal cancer (CRC) is the second most prevalent form of cancer in the United States, according to the American Cancer Society, and the standard of care for the treatment of CRC relies upon continuous chemotherapy infusions delivered via electronic ambulatory infusion pumps.

The Company provides these pumps and related supplies to oncology clinics, obtains an assignment of insurance benefits from the patient, and bills the patient’s insurance company or patient as appropriate, for the use of the pump and supplies, and collects payment. The Company provides pump management services for the pumps and associated disposable supply kits to over 1,300 oncology practices in the United States. The Company retains title to the pumps during this process.

In addition, the Company sells, rents and leases new and pre-owned pole mounted and ambulatory infusion pumps to, and provides biomedical certification, maintenance and repair services for, these same oncology practices as well as to other alternate site settings including home care and home infusion providers, skilled nursing facilities, pain centers and others in the United States and Canada. The Company also provides these products and services to customers in the hospital market.

The Company purchases new and pre-owned pole mounted and ambulatory infusion pumps from a variety of sources on a non-exclusive basis. The Company repairs, refurbishes and provides biomedical certification for the devices as needed. The pumps are then available for sales, rental or to be used within the Company’s ambulatory infusion pump management service.

2

One aspect of our business strategy over the next one to three years is to expand into treatment of other cancers. We currently generate approximately 20% of our revenue from treatments for disease states other than colorectal cancer. There are a number of approved treatment regimens for head and neck, pancreatic, esophageal and other gastric cancers which present opportunities for growth. There are also a number of other drugs currently approved by the U.S. Food and Drug Administration (the FDA), as well as agents in the pharmaceutical development pipeline, which we believe could potentially be used with continuous infusion protocols for the treatment of other diseases in addition to colorectal cancer. Drugs or protocols currently in clinical trials may also obtain regulatory approval over the next several years. If these new drugs obtain regulatory approval for use with continuous infusion protocols, we expect the pharmaceutical companies to focus their sales and marketing forces on promoting the new drugs and protocols to physicians.

Another aspect of our business strategy over the next one to three years is to actively pursue opportunities for the expansion of our business through strategic alliances, joint ventures and/or acquisitions. We believe there are opportunities to acquire smaller, regional competitors that perform similar services to us, but do not have the national market access, a network of third party payor contracts or operating economies of scale that we currently enjoy. We also plan to leverage our extensive networks of oncology practices and insurers by distributing complementary products and introducing key new services.

We face risks that other competitors can provide the same services as us. Those risks are currently mitigated by our existing third party payor contracts and economies of scale, which allow for predictable reimbursement and less costly purchase and management of the pumps, respectively. Additionally, we have already established a long standing relationship as a provider of pumps to over 1,300 oncology practices in the United States. We believe that there are competitive barriers to entry against other suppliers with respect to these oncology practices because we have an established national presence and third party payor contracts in place covering approximately 195 million third party payor lives (i.e., persons enrolled in various managed care plans or commercial insurance carriers such as health maintenance organizations and preferred provider organizations) increasing the likelihood that we participate in the insurance networks of patients to whom physicians wish to refer an ambulatory infusion pump provider. Moreover, we have an available inventory of approximately 21,000 active ambulatory infusion pumps, which may allow us to be more responsive to the needs of physicians and patients than a new market entrant. We do not perform any research and development.

First Biomedical

On June 15, 2010, we acquired all of the issued and outstanding stock of First Biomedical, Inc (First Biomedical) pursuant to a Stock Purchase Agreement with the stockholders of First Biomedical.

First Biomedical sells, rents, services and repairs new and pre-owned infusion pumps and other medical equipment. It also sells a variety of primary and secondary tubing, cassettes, catheters and other disposable items that are utilized with infusion pumps. Headquartered in Olathe, Kansas, with additional facilities in California and Toronto, First Biomedical is a leading provider to alternate site healthcare facilities and hospitals in the United States and Canada. The acquisition of First Biomedical has allowed us to expand our offerings to existing customers with the addition of biomedical service and repair, while simultaneously bolstering the growth of infusion pump sales within our existing and potential future markets.

First Biomedical’s results of operations are included in our consolidated statements of operations from the date of acquisition.

Continuous Infusion Therapy

Continuous infusion of chemotherapy involves the gradual administration of a drug via a small, lightweight, portable electronic infusion pump over a prolonged period of time, defined as greater than 8 hours, and up to 24 hours daily. A cancer patient can receive his or her medicine anywhere from 1 to 30 days per month depending

3

on the chemotherapy regimen that is most appropriate to that individual’s health status and disease state. This may be followed by periods of rest and then repeated cycles with treatment goals of progression free disease survival. This drug administration method has replaced intravenous push or bolus administration in specific circumstances. The advantages of slow continuous low doses of certain drugs are well documented. Clinical studies support the use of continuous infusion chemotherapy for decreased toxicity without loss of anti-tumor efficacy. The 2009/2010 National Comprehensive Cancer Network (NCCN) Guidelines recommend the use of continuous infusion for treatment of numerous cancer diagnoses. We believe that the growth of continuous infusion therapy is driven by three factors: evidence of improved clinical outcomes; lower toxicity and side effects; and a favorable reimbursement environment.

| • | In the past decade, significant progress has been made in the treatment of colorectal cancer due to advances in surgery, radiotherapy and chemotherapy. In the late 1990s, medical researchers discovered that the delivery method of the drug (or schedule) was a key component to drug availability, efficacy and tolerability. Schedule dependant anti-tumor activity and toxicity has resulted in continuous infusion 5-Fluorouracil being adopted as the standard of care. In 2000, the FDA approved Camptosar (the trade name for the generic chemotherapy drug Irinotecan), a drug developed by Pfizer, for first-line therapy in combination with 5-Fluorouracil for the treatment of colorectal cancer. In 2002, the FDA approved Eloxatin (the trade name for the generic chemotherapy drug Oxaliplatin), a drug developed by Sanofi-Aventis, for use in combination with continuous infusion 5-Fluorouracil for the treatment of colorectal cancer. FOLFIRI, the chemotherapy protocol which includes Camptosar in combination with continuous infusion 5-Fluorouracil and the drug Leucovorin, and FOLFOX, the chemotherapy protocol which includes Eloxatin in combination with continuous infusion 5-Fluorouracil and Leucovorin, have resulted in significantly improved overall survival rates for colorectal cancer patients at various stages of the disease state. We believe that Sanofi-Aventis and Pfizer have each dedicated significant resources to educating physicians and promoting the use of FOLFOX and FOLFIRI. Simultaneously, the NCCN has established these regimens as the standards of care for the treatment of colorectal cancer. |

| • | The use of continuous infusion has been demonstrated to decrease or alter the toxicity of a number of cytotoxic, or cell killing agents. Higher doses of drugs can be infused over longer periods of time, leading to improved tolerance and decreased toxicity. For example, the cardiotoxicity (heart muscle damage) of the chemotherapy drug Doxorubicin is decreased by schedules of administration (The Chemotherapy Source Book, Perry, M.C.). Nausea, vomiting, diarrhea and decreased white blood cell and platelet counts are all affected by duration of delivery. Continuous infusion can lead to improved tolerance and patient comfort while enhancing the patient’s ability to remain on the chemotherapy regimen. Additionally, the lower toxicity profile and resulting reduction in side effects enables patients undergoing continuous infusion therapy to continue a relatively normal lifestyle, which may include continuing to work, go shopping, and care for family members. We believe that the partnering of physician management and patient autonomy provide for the highest quality of care with the greatest patient satisfaction. |

| • | We believe that oncology practices have a heightened sensitivity to whether and how much they are reimbursed for services. Simultaneously, the Center for Medicare and Medicaid Services (CMS) and private insurers are increasingly focusing on evidenced based medicine to inform their reimbursement decisions — that is, aligning reimbursement with clinical outcomes and adherence to standards of care. Continuous infusion therapy is a main component of the standard of care for certain cancer types because clinical evidence demonstrates superior outcomes. Payors recognize this and it is reflected in favorable reimbursement for clinical services related to the delivery of this care. |

Services

Our core service is to provide oncology offices, infusion clinics and hospital out-patient chemotherapy clinics with ambulatory infusion pumps in addition to related supplies for patient use. We then directly bill and collect payment from payors and patients for the use of these pumps. We own approximately 21,000 ambulatory

4

infusion pumps which are dedicated to this service offering. At any given time, it is estimated that approximately 60% of the pumps are in the possession of patients. The remainder of the pumps is in transport for cleaning and calibration, or in oncology clinics as back-ups.

After a doctor determines that a patient is eligible for ambulatory infusion pump therapy, the doctor arranges for the patient to receive an infusion pump and provides the necessary chemotherapy drugs. The oncologist and nursing staff train the patient in the use of the pump and initiate service. The physician bills insurers, Medicare, Medicaid, third party payor companies or patients (collectively, “payors”) for the physician’s professional services associated with initiating and supervising the infusion pump administration, as well as the supply of drugs. We directly bill payors for the use of the pump and related disposable supplies. We have contracts with more than 200 payors that cover approximately 195 million third party payor lives. Billing to payors requires coordination with patients and physicians who initiate the service, as physicians’ offices must provide us with appropriate paperwork (patient’s insurance information, physician’s order and an acknowledgement of benefits that shows receipt of equipment by the patient) in order for us to bill the payors.

In addition to providing high quality and convenient care, we believe that our business offers significant economic benefits for patients, providers and payors.

| • | We provide patients with 24-hour by 7 days (24x7) service and support. We employ oncology and intravenous certified registered nurses trained on ambulatory infusion pump equipment who staff our 24x7 hotline to address questions that patients may have about their pump treatment, the infusion pumps or other medical or technical questions related to the pumps. |

| • | Physicians use our services to outsource the capital commitment, pump service, maintenance and billing and administrative burdens associated with pump ownership. Our service also allows the doctor to continue a direct relationship with the patient and to receive professional service fees for setting up the treatment and administering the drugs. |

| • | We believe our services are attractive to payors because they are generally less expensive than hospitalization or home care. |

Other services we offer include the sales, rental and leasing of pole mounted and ambulatory infusion pumps to oncology practices, hospitals and other clinical settings. We own a fleet of approximately 14,000 new and used pole mounted and ambulatory pumps, representing over 70 makes and models of equipment which are dedicated to these services. These pumps are available for daily, weekly, monthly or annual rental periods as well as for sale or lease.

In addition to sales, rental and leasing services, the company also provides biomedical maintenance, repair and certification services for the devices we provide as well as for devices owned by customers but not acquired through InfuSystem. We operate pump service and repair Centers of Excellence across the United States and Canada and employ a staff of highly trained technicians to provide these services.

Relationships with Physician Offices

We have business relationships with clinical oncologists in more than 1,300 practices. Though this represents a substantial portion of the oncologists in the United States, we believe we can continue to expand our network to further penetrate the oncology market. Based on our high retention rates and the positive results of our professional customer satisfaction research, we believe our relationships with physician offices are strong.

We believe that, in general, we do not compete directly with hospitals and physician offices to treat patients. Rather, by providing products and services to hospitals and physician offices and other care facilities and providers, we believe that we assist other providers in meeting increasing patient demand and manage institutional constraints on capital and manpower due to the nature of limited resources in hospitals and physician offices.

5

Sales and Marketing

We employ a sales team of approximately 39 salespersons to coordinate our sales and marketing activities. Our efforts are directed primarily at physician’s offices, infusion clinics, hospital outpatient chemotherapy clinics and other enterprises serving patients who receive continuous infusions.

Employees

As of December 31, 2010, we had 180 employees, including 167 full-time employees and 13 part-time employees. None of our employees are unionized.

Company Officers

Sean McDevitt, Chairman and Chief Executive Officer

Mr. McDevitt has served as the Company’s Chairman of the Board since April 2005 and as Chief Executive Officer since September 2009. Mr. McDevitt is a founding principal, and since 2007 has been a Managing Director of Maren Group, an investment banking firm which provides mergers and acquisitions advisory services in the healthcare and technology sectors. Prior to joining Maren Group, Mr. McDevitt was a Managing Director of FTN Midwest Securities Corp. from September 2004 to January 2007. In 1999, Mr. McDevitt co-founded Alterity Partners, a boutique investment bank which provided capital markets and merger and acquisition advisory services to high growth companies. Alterity Partners was acquired by FTN Midwest Securities Corp. in September 2004. Mr. McDevitt was formerly a senior investment banker at Goldman Sachs & Company, from 1995 through 1999 where he led deal teams in a variety of technology and healthcare/biopharmaceutical transactions, including mergers and acquisitions, divestitures and initial public offerings. Prior to Goldman Sachs & Company, Mr. McDevitt worked in sales and marketing at Pfizer Inc. from 1991 until 1994. He was a Captain in the U.S. Army Rangers and was decorated for combat in the Panama invasion. He is a member of the Council on Foreign Relations. Mr. McDevitt received his B.S. in Computer Science and Electrical Engineering from the U.S. Military Academy at West Point and an M.B.A. from Harvard Business School.

James M. Froisland, Chief Financial Officer

Mr. Froisland has served as the Company’s Chief Financial Officer since December 2010. Prior to joining InfuSystem, from 2006 to 2010, Mr. Froisland served as Senior Vice President, Chief Financial Officer, Chief Information Officer and Corporate Secretary for Material Sciences Corporation (NASDAQ:MASC). Prior to this role, Mr. Froisland served as Senior Vice President, Chief Financial Officer and Chief Information Officer for InteliStaf Healthcare, Inc. and has held a variety of c-level and senior financial and information technology positions at Burns International Services Corporation, Anixter International Inc., Budget Rent A Car Corporation, Allsteel Inc., and The Pillsbury Company. Mr. Froisland started his career with KPMG, LLP and is a Certified Public Accountant. Mr. Froisland has an MBA, in Management Information Systems from the Carlson School of Management, University of Minnesota, and a BA, in Math and Accounting, from Luther College. Mr. Froisland also serves on the Board of Directors and Audit Committee for Westell Technologies, Inc. (NASDAQ:WSTL).

Material Suppliers

We supply a wide variety of pumps and associated equipment, as well as disposables and ancillary supplies. The majority of our pumps are electronic ambulatory pumps purchased from the following manufacturers, each of which is material and supplies more than 10% of the ambulatory pumps purchased by us: Smiths Medical, Inc.; Hospira Worldwide, Inc.; and WalkMed Infusion, LLC (formerly known as McKinley Medical, LLC). There are no supply agreements in place with any of the suppliers. All purchases are handled pursuant to pricing agreements, which contain no material terms other than prices that are subject to change by the manufacturer.

Seasonality

Our business is not subject to seasonality.

6

Environmental Laws

We are required to comply with applicable environmental laws regulating the disposal of cleaning agents used in the process of cleaning our ambulatory infusion pumps, as well as the disposal of sharps and blood products used in connection with the pumps. We do not believe that compliance with such laws has a material effect on our business.

Significant Customers

We have sought to establish contracts with as many third party payor organizations as commercially practicable, in an effort to ensure that reimbursement is not a significant obstacle for providers who recommend continuous infusion therapy and wish to utilize our services. A third party payor organization is a health care payor or a group of medical services payors that contracts to provide a wide variety of healthcare services to enrolled members through participating providers such as us. A payor is any entity that pays on behalf of a member patient.

We currently have contracts with more than 200 third party payor plans that cover approximately 195 million lives. Material terms of contracts with third party payor organizations are typically a set fee or rate, or discount from billed charges for equipment provided. These contracts generally provide for a term of one year, with automatic one-year renewals, unless we or the contracted payor do not wish to renew. Our largest contracted payor is Medicare, which accounted for approximately 31% of our gross billings for ambulatory infusion pump services for the year ended December 31, 2010. Our contracts with various individual Blue Cross/Blue Shield affiliates in the aggregate accounted for approximately 23% of our gross billings for ambulatory infusion pump services for the year ended December 31, 2010. We also contract with various other third party payor organizations, commercial Medicare replacement plans, self insured plans and numerous other insurance carriers. No individual payor, other than Medicare and the Blue Cross/Blue Shield entities, accounts for greater than approximately 6% of our ambulatory infusion pump services gross billings.

Competitors

We believe that our competition is primarily composed of regional providers, hospital-owned durable medical equipment (DME) providers, physician providers and home care infusion providers. An estimate of the number of competitors is not known or reasonably available, due to the wide variety in type and size of the market participants described below. We are not aware of any industry reports with respect to the competitive market described below. The description of market segments and business activities within those market segments is based on our experiences in the industry.

| • | Regional Providers: Regional DME providers act as distributors for a variety of medical products. We believe regional DME provider sales forces generally consist of a relatively small number of salespeople, usually covering several states. Regional DME providers tend to carry a limited selection of infusion pumps and their salespeople generally have limited resources. Regional DME providers usually do not have 24x7 nursing services. We believe that regional DME providers have relatively few third party payor contracts, which may prevent these providers from being paid at acceptable levels and may also result in higher out-of-pocket costs for patients. |

| • | Hospital-owned DME Providers: Many hospitals have in-house DME providers to supply basic equipment. In general, however, these providers have limited capital and tend to stock a small inventory of infusion pumps. We believe that hospital-owned providers have limited ability to grow because of restricted patient populations. Growth from outside of the hospital may pose a challenge because hospitals typically will not provide referrals to competitors, instead preferring to offer patients a choice of non-hospital-affiliated DME providers. |

| • | Physician Providers: A limited number of physicians maintain an inventory of their own infusion pumps and provide them to patients for a fee. However, we believe that pump utilization in this area |

7

| tends to be low and the costs associated with ongoing supplies, preventative maintenance and repairs can be relatively high. Moreover, we believe that a high percentage of DME claims by doctors are rejected by payors upon first submission, requiring a physician’s staff to spend significant time and effort to resubmit claims and receive payment for treatment. The numerous service and technical questions from patients may present another significant cost to a physician provider’s staff. |

| • | Home Care Infusion Providers: Home care infusion providers provide chemotherapy drugs and services to allow for in-home patient treatment. We believe that home care infusion treatment can be very costly and that many patients do not carry insurance coverage that covers home-based infusion services, resulting in larger out-of-pocket costs. Because home care treatments may take as long as six months, these costs can be high and can result in higher patient co-payments. We believe that home care providers may also be reluctant to offer 24x7 coverage or additional patient visits, due to capped fees. |

Regulation of Our Business

Our business is subject to certain regulations. Specifically, as a Medicare supplier of DME and related supplies, we must comply with DMEPOS Supplier Standards established by the Health Care Financing Administration regulating Medicare suppliers of DME and prosthetics, orthotics and supplies (DMEPOS). The DMEPOS Supplier Standards consist of 26 requirements that must be met in order for a DMEPOS supplier to be eligible to receive payment for a Medicare-covered item. Some of the more significant DMEPOS Supplier Standards require us to (i) advise Medicare beneficiaries of their option to purchase certain equipment, (ii) honor all warranties under state law and not charge Medicare beneficiaries for the repair or replacement of equipment or for services covered under warranty, (iii) permit agents of the Centers for Medicare and Medicaid Services to conduct on-site inspections to ascertain compliance with the DMEPOS Supplier Standards, (iv) maintain liability insurance in prescribed amounts, (v) refrain from contacting Medicare beneficiaries by telephone, except in certain limited circumstances, (vi) answer questions and respond to complaints of beneficiaries regarding the supplied equipment, (vii) disclose the DMEPOS Supplier Standards to each Medicare beneficiary to whom we supply equipment, (viii) maintain a complaint resolution procedure and record certain information regarding each complaint, (ix) maintain accreditation from a CMS approved accreditation organization and, (x) meet the surety bond requirements specified in 42 C.F.R. 424.57.

We are also subject to the provisions of the Health Insurance Portability and Accountability Act of 1996 (HIPAA) which are designed to protect the security and confidentiality of certain patient health information. Under HIPAA, we must provide patients access to certain records and must notify patients of our use of personal medical information and patient privacy rights. Moreover, HIPAA sets limits on how we may use individually identifiable health information and prohibits the use of patient information for marketing purposes. The adoption of the American Recovery and Reinvestment Act of 2009 (ARRA) includes a new breach notification requirement that applies to breaches of unsecured health information occurring on or after September 23, 2009.

We are subject to regulation in the various states in which we operate. We believe we are in compliance with all such regulation.

The healthcare industry is undergoing fundamental changes resulting from political, economic and regulatory influences. In the U.S., comprehensive programs are under consideration that seek to, among other things, increase access to healthcare for the uninsured and control the escalation of healthcare expenditures within the economy. On March 23, 2010, healthcare reform legislation (the “Healthcare Legislation”) was approved by Congress and has been signed into law. This legislation has only recently been enacted and requires the adoption of implementing regulations, which may impact our business.

Available Information

Our Internet address is www.infusystem.com. On this Web site, we post the following filings as soon as reasonably practicable after they are electronically filed with or furnished to the U.S. Securities and Exchange

8

Commission (the SEC): our Annual Reports on Form 10-K; our Quarterly Reports on Form 10-Q; our Current Reports on Form 8-K; our proxy statements related to our annual stockholders’ meetings; and any amendments to those reports or statements. All such filings are available on our Web site free of charge. The content on our Web site is not incorporated by reference into this Annual Report on Form 10-K unless expressly noted.

| Item 1A. | Risk Factors. |

An investment in our securities involves a high degree of risk. You should consider carefully all of the material risks described below, together with the other information contained in this Annual Report on Form 10-K. If any of the following events occur, our business, financial condition, results of operations and cash flows may be materially adversely affected.

RISK FACTORS RELATING TO OUR BUSINESS AND THE INDUSTRY IN WHICH WE OPERATE.

We are dependent on our Medicare Supplier Number.

We are required to have a Medicare Supplier Number in order to bill Medicare for services provided to Medicare patients. Furthermore, all third party and Medicaid contracts require us to have a Medicare Supplier Number. In addition, we are required to comply with Medicare Supplier Standards in order to maintain such number. If we are unable to comply with the relevant standards, we could lose our Medicare Supplier Number. The loss of such identification number for any reason would prevent us from billing Medicare for patients who rely on Medicare to pay their medical expenses and, as a result, we would experience a decrease in our revenues. Without such a number, we would be unable to continue our various third party and Medicaid contracts. A significant portion of our revenue is dependent upon our Medicare Supplier Number.

The Center for Medicare and Medicaid Services (CMS) has issued a ruling that all durable medical equipment (“DME”) providers must be accredited by a recognized accrediting entity by September 30, 2009. On February 17, 2009, we received accreditation from Community Health Accreditation Program (CHAP), thus meeting this CMS requirement. If we lost our accredited status, our financial condition, revenues and results of operations would be materially and adversely affected.

Changes in third-party reimbursement rates may adversely impact our revenues.

Our revenues are substantially dependent on third-party reimbursement. We are paid directly by private insurers and governmental agencies, often on a fixed fee basis, for continuous infusion equipment and related disposable supplies provided to patients. If the average fees allowable by private insurers or governmental agencies were reduced, the negative impact on revenues could have a material adverse effect on our financial condition, results of operations and cash flows. Also, if amounts owed to us by patients and insurers are reduced or not paid on a timely basis, we may be required to increase our bad debt expense and/or decrease our revenues.

Any change in the overall healthcare reimbursement system may adversely impact our business.

Changes in the healthcare reimbursement system often create financial incentives and disincentives that encourage or discourage the use of a particular type of product, therapy or clinical procedure. Market acceptance of continuous infusion therapy may be adversely affected by changes or trends within the healthcare reimbursement system. Changes to the health care reimbursement system that favor other technologies or treatment regimens that reduce reimbursements to providers or treatment facilities that use our services, may adversely affect our ability to market our services profitably.

9

Our success is impacted by the availability of the chemotherapy drugs that are used in our continuous infusion pump systems.

We primarily derive our revenue from the rental of ambulatory infusion pumps to oncology patients through physicians’ offices and chemotherapy clinics. A shortage in the availability of chemotherapy drugs that are used in the continuous infusion pump system could have a material adverse effect on our financial condition, results of operations and cash flows.

If future clinical studies demonstrate that oral medications are as effective as or more effective than continuous infusion therapy, our business could be adversely affected.

Numerous clinical trials are currently ongoing, evaluating and comparing the therapeutic benefits of current continuous infusion-based regimens with various oral medication regimens. If these clinical trials demonstrate that oral medications provide equal or greater therapeutic benefits and/or demonstrate reduced side effects compared to prior oral medication regimens, our revenues and overall business could be materially and adversely affected. Additionally, if new oral medications are introduced to the market that are superior to existing oral therapies, physicians’ willingness to prescribe continuous infusion-based regimens could decline, which would adversely affect our financial condition, results of operations and cash flows.

Global financial conditions may negatively impact our business, results of operations, financial condition and/or liquidity.

The recent global financial crisis affecting the banking system and financial markets, as well as the uncertainty in global economic conditions, have resulted in a significant tightening of credit markets, a low level of liquidity in financial markets and reduced corporate profits and capital spending. As a result, our customers (i.e., patients and payors) may face issues gaining timely access to sufficient credit, which could result in an impairment of their ability to make timely payments to us. In addition, the current global financial crisis could also adversely impact our suppliers’ ability to provide us with materials and components, either of which may negatively impact our financial condition, results of operations and cash flows. The financial crisis could also adversely impact our ability to access the financial markets.

Although we maintain allowances for doubtful accounts for estimated losses resulting from the inability of our customers to make required payments and such losses have historically been within our expectations and the provisions established, we cannot guarantee that we will continue to experience the same loss rates that we have in the past, especially given the current turmoil of the worldwide economy.

State licensure laws for durable medical equipment, or DME, suppliers are subject to change. If we fail to comply with any state’s laws, we will be unable to operate as a DME supplier in such state and our business operations will be adversely affected.

As a DME supplier operating in all 50 states of the United States, we are subject to each state’s licensure laws regulating DME suppliers. State licensure laws for DME suppliers are subject to change and we must ensure that we are continually in compliance with the laws of all 50 states. In the event that we fail to comply with any state’s laws governing the licensing of DME suppliers, we will be unable to operate as a DME supplier in such state until we regain compliance. We may also be subject to certain fines and/or penalties and our business operations could be adversely affected.

Our growth strategy includes expanding into treatment for cancers other than colorectal. There can be no assurance that continuous infusion-based regimens for these other cancers will become standards of care for large numbers of patients or that we will be successful in penetrating these different markets.

An aspect of our growth strategy is to expand into the treatment of other cancers, such as head, neck and gastric. Currently, relatively small percentages of these patients are treated with regimens that include continuous infusion therapy. That population will expand only if clinical trial results for new drugs and new combinations of

10

drugs demonstrate superior outcomes for regimens that include continuous infusion therapy relative to alternatives. No assurances can be given that these new drugs and drug combinations will be approved or will prove superior to oral medication or other treatment alternatives. In addition, no assurances can be given that we will be able to penetrate successfully any new markets that may develop in the future or manage the growth in additional resources that would be required.

The industry in which we operate is intensely competitive and changes rapidly. If we are unable to successfully compete with our competitors, our business operations may suffer.

The drug infusion industry is highly competitive. Some of our competitors and potential competitors have significantly greater resources than we do for research and development, marketing and sales. As a result, they may be better able to compete for market share, even in areas in which our services may be superior. The industry is subject to technological changes and such changes may put our current fleet of pumps at a competitive disadvantage. If we are unable to effectively compete in our market, our financial condition, results of operations and cash flows may materially suffer.

Our industry is dependent on regulatory guidelines that affect our billing practices. If our competitors do not comply with these regulatory guidelines, our business could be adversely affected.

Aggressive competitors may not fully comply with rules pertaining to documentation required by CMS and other payors for patient billing. Competitors, who don’t meet the same standards of compliance that we do with regards to billing regulations, can put us at a potential competitive disadvantage. We are a participating provider with Medicare and under contract with more than 200 additional insurance plans, all of which have very stringent guidelines. If our competitors do not comply with these regulatory guidelines, our business could be adversely affected.

We rely on independent suppliers for our products. Any delay or disruption in the supply of products, particularly our supply of electronic ambulatory pumps, may negatively impact our operations.

Our infusion pumps are obtained from outside vendors. The majority of our new pumps are electronic ambulatory infusion pumps which are supplied to us by three major suppliers: Smiths Medical, Inc.; Hospira Worldwide, Inc.; and WalkMed Infusion, LLC (formerly known as McKinley Medical, LLC). The loss or disruption of our relationships with outside vendors could subject us to substantial delays in the delivery of pumps to customers. Significant delays in the delivery of pumps could result in possible cancellation of orders and the loss of customers. Our inability to provide pumps to meet delivery schedules could have a material adverse effect on our reputation in the industry, as well as our financial condition, results of operations and cash flows.

Although we do not manufacture the products we distribute, if one of the products distributed by us proves to be defective or is misused by a health care practitioner or patient, we may be subject to liability that could adversely affect our financial condition and results of operations.

Although we do not manufacture the pumps that we distribute, a defect in the design or manufacture of a pump distributed by us, or a failure of pumps distributed by us to perform for the use specified, could have a material adverse effect on our reputation in the industry and subject us to claims of liability for injuries and otherwise. Misuse of the pumps distributed by us by a practitioner or patient that results in injury could similarly subject us to liability. Any substantial underinsured loss could have a material adverse effect on our financial condition, results of operations and cash flows. Furthermore, any impairment of our reputation could have a material adverse effect on our revenues and prospects for future business.

11

Unexpected costs or delays in integrating acquisitions could adversely affect our financial results.

During the year the Company acquired all of the outstanding stock of First Biomedical, and plans to make additional acquisitions going forward . As a result, we must devote significant management attention and resources to integrating the business practices and operations . We may encounter difficulties that could harm the businesses, adversely affect our financial condition, and cause our stock price to decline, including the following:

| • | We may have difficulty or experience delays in integrating the business and operations; |

| • | We may have difficulty maintaining employee morale and retaining key managers and other employees as we take steps to combine the personnel and business cultures of separate organizations into one, and to eliminate duplicate positions and functions; and |

| • | We may have difficulty preserving important relationships with others, such as strategic partners, customers, and suppliers, who may delay or defer decisions on agreements with us, or seek to change existing agreements with us, because of the acquisition. |

The integration process may divert the attention of our officers and management from day-to-day operations and disrupt our business, particularly if we encounter these types of difficulties. The failure of the combined company to meet the challenges involved in the integration process could cause an interruption of or a loss of momentum in the activities of the combined company and could seriously harm our results of operations.

Even if the operations are integrated successfully, the combined company may not fully realize the expected benefits of the transaction, including the synergies, cost savings or growth opportunities, whether within the anticipated time frame, or anytime in the future.

We intend to actively pursue opportunities for the further expansion of our business through strategic alliances, joint ventures and/or acquisitions. Future strategic alliances, joint ventures and/or acquisitions may require significant resources and/or result in significant unanticipated costs or liabilities to us.

Over the next two to three years we intend to actively pursue opportunities for the further expansion of our business through strategic alliances, joint ventures and/or acquisitions. Any future strategic alliances, joint ventures or acquisitions will depend on our ability to identify suitable partners or acquisition candidates, as the case may be, negotiate acceptable terms for such transactions and obtain financing, if necessary. We also face competition for suitable acquisition candidates which may increase our costs. Acquisitions or other investments require significant managerial attention, which may be diverted from our other operations. Any future acquisitions of businesses could also expose us to unanticipated liabilities.

If we engage in strategic acquisitions, we may experience significant costs and difficulty in assimilating operations or personnel, which could threaten our future growth.

If we make any acquisitions, we could have difficulty assimilating operations, technologies and products or integrating or retaining personnel of acquired companies. In addition, acquisitions may involve entering markets in which we have no or limited direct prior experience. The occurrence of any one or more of these factors could disrupt our ongoing business, distract our management and employees and increase our expenses. In addition, pursuing acquisition opportunities could divert our management’s attention from our ongoing business operations and result in decreased operating performance. Moreover, our profitability may suffer because of acquisition-related costs or amortization of intangible assets. Furthermore, we may have to incur debt or issue equity securities in future acquisitions. The issuance of equity securities would dilute our existing stockholders.

Covenants in our debt agreements restrict our business.

The credit agreement that governs our credit facility with Bank of America, N.A. and KeyBank National Association contains, and the agreements that govern our future indebtedness may contain, covenants that restrict our ability to and the ability of our subsidiaries to, among other things:

| • | create, incur, assume or suffer to exist any lien upon any of our property, assets or revenues; |

12

| • | make certain investments; |

| • | create, incur, assume or suffer to exist any indebtedness; |

| • | merge, dissolve, liquidate, consolidate all or substantially all of our assets; |

| • | make any disposition or enter into any agreement to make any disposition; and |

| • | declare or make, directly or indirectly, any dividend or other restricted payment, or incur any obligation (contingent or otherwise) to do so. |

Recently adopted healthcare reform legislation may adversely affect our business.

The healthcare industry is undergoing fundamental changes resulting from political, economic and regulatory influences. In the U.S., comprehensive programs are under consideration that seek to, among other things, increase access to healthcare for the uninsured and control the escalation of healthcare expenditures within the economy. On March 23, 2010, healthcare reform legislation (the “Healthcare Legislation”) was approved by Congress and has been signed into law. This legislation has only recently been enacted and requires the adoption of implementing regulations, which may impact our business. The Healthcare Legislation could have a material adverse effect on our business, financial condition and results of operations.

If we fail to comply with applicable healthcare regulations, we could face substantial penalties and our business, operations and financial condition could be adversely affected.

Certain federal and state healthcare laws and regulations pertaining to fraud and abuse and patients’ rights may be applicable to our business. We may be subject to healthcare fraud and abuse regulation and patient privacy regulation by both the federal government and the states in which we conduct our business. The laws that may affect our ability to operate include:

| • | the federal healthcare program Anti-Kickback Statute, which prohibits, among other things, soliciting, receiving or providing remuneration, directly or indirectly, to induce (i) the referral of an individual, for an item or service, or (ii) the purchasing or ordering of a good or service, for which payment may be made under federal healthcare programs such as the Medicare and Medicaid programs; |

| • | federal false claims laws which prohibit, among other things, knowingly presenting, or causing to be presented, claims for payment from Medicare, Medicaid, or other third-party payors that are false or fraudulent, and which may apply to entities like us that promote medical devices, provide medical device management services and may provide coding and billing advice to customers; |

| • | the federal Health Insurance Portability and Accountability Act of 1996, or HIPAA, which prohibits executing a scheme to defraud any healthcare benefit program or making false statements relating to healthcare matters and which also imposes certain requirements relating to the privacy, security and transmission of individually identifiable health information; and |

| • | state law equivalents of each of the above federal laws, such as anti-kickback and false claims laws that may apply to items or services reimbursed by any third-party payor, including commercial insurers, and state laws governing the privacy and security of health information in certain circumstances, many of which differ in significant ways from state to state and often are not preempted by HIPAA, thus complicating compliance efforts. |

Additionally, the compliance environment is changing, with more states, such as California and Massachusetts, mandating implementation of compliance programs, compliance with industry ethics codes, and spending limits, and other states, such as Vermont, Maine, and Minnesota, requiring reporting to state governments of gifts, compensation and other remuneration to physicians. Federal legislation, the Physician Payments Sunshine Act of 2009, has been proposed and is moving forward in Congress. This legislation would require disclosure to the federal government of payments to physicians. These laws all provide for penalties for

13

non-compliance. The shifting regulatory environment, along with the requirement to comply with multiple jurisdictions with different compliance and reporting requirements, increases the possibility that a company may run afoul of one or more laws.

If our operations are found to be in violation of any of the laws described above or any other governmental regulations that apply to us, we may be subject to penalties, including civil and criminal penalties, damages, fines and the curtailment or restructuring of our operations. Any penalties, damages, fines, curtailment or restructuring of our operations could adversely affect our ability to operate our business and our financial results. Any action against us for violation of these laws, even if we successfully defend against it, could cause us to incur significant legal expenses and divert our management’s attention from the operation of our business. Moreover, achieving and sustaining compliance with applicable federal and state privacy, security and fraud laws may prove costly.

We are dependent on key personnel, and the loss of any key employees or officers may have a materially adverse effect on our operations.

Our success is substantially dependent on the continued services of our executive officers and other key personnel who generally have extensive experience in our industry. Our future success also will depend in large part upon our ability to identify, attract and retain other highly qualified managerial, technical and sales and marketing personnel. Competition for these individuals is intense. The loss of the services of any key employees, or our failure to attract and retain other qualified and experienced personnel on acceptable terms, could have a material adverse effect on our business and results of operations.

The preparation of our financial statements in accordance with accounting principles generally accepted in the United States requires us to make estimates, judgments, and assumptions that may ultimately prove to be incorrect.

The accounting estimates and judgments that management must make in the ordinary course of business affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the periods presented. If management misinterprets GAAP, subsequent adjustments resulting from errors could have a material adverse effect on our operating results for the period or periods in which the change is identified. Additionally, subsequent adjustments from errors could require us to restate our financial statements. Restating financial statements could result in a material decline in the price of our stock.

RISK FACTORS RELATING SPECIFICALLY TO OUR COMMON STOCK AND WARRANTS

The market price of our common stock has been, and is likely to remain, volatile and may decline in value.

The market price of our common stock has been and is likely to continue to be volatile. Market prices for securities of healthcare services companies, including ours, have historically been volatile, and the market has from time to time experienced significant price and volume fluctuations that appear unrelated to the operating performance of particular companies. The following factors, among others, can have a significant effect on the market price of our securities:

| • | announcements of technological innovations, new products, or clinical studies by others; |

| • | government regulation; |

| • | changes in the coverage or reimbursement rates of private insurers and governmental agencies; |

| • | announcements regarding new products or services or strategic alliances or acquisitions; |

| • | developments in patent or other proprietary rights; |

| • | the liquidity of the market for our common stock and warrants; |

14

| • | changes in health care policies in the United States or globally; |

| • | global financial conditions; and |

| • | comments by securities analysts and general market conditions. |

The realization of any risks described in these “Risk Factors” could also have a negative effect on the market price of our common stock and warrants.

We do not pay dividends and this may negatively affect the price of our stock.

Under the terms of our credit agreement with Bank of America, N.A. and KeyBank National Association, we are not permitted to pay dividends on our common stock and do not anticipate paying dividends on our common stock in the foreseeable future. The future price of our common stock may be adversely impacted because we do not pay dividends.

Future sales of our common stock may depress our stock price.

The market price of our common stock could decline as a result of sales of substantial amounts of our common stock in the public market, or the perception that these sales could occur. In addition to the shares of our common stock currently available for sale in the public market, shares of our common stock sold in past private placements (which include shares held by certain members of our board of directors) and the shares of common stock underlying our outstanding warrants are subject to registration rights. If the holders of these securities choose to exercise their registration rights, this would result in an increase in the number of shares of our common stock available for resale in the public market, which in turn could lead to a decrease in our stock price and a dilution of stockholders’ ownership interests. These factors could also make it more difficult for us to raise funds through future equity offerings.

Certain anti-takeover provisions in our amended and restated certificate of incorporation and bylaws and the Delaware General Corporation Law (the DGCL,), as well as our stockholders rights plan, may discourage, delay or prevent a change in control of our company and adversely affect the trading price of our common stock.

Our amended and restated certificate of incorporation and bylaws and the DGCL contain certain anti-takeover provisions which may discourage, delay or prevent a change in control of our company that our stockholders may consider favorable and, as a result, adversely affect the trading price of our common stock. Our amended and restated certificate of incorporation authorizes our board of directors to issue up to 1,000,000 shares of blank check preferred stock. Our amended and restated bylaws include provisions establishing advance notice procedures with respect to stockholder proposals and director nominations and permitting only stockholders holding at least a majority of our outstanding common stock to call a special meeting. Additionally, as a Delaware corporation, we are subject to section 203 of the DGCL, which, among other things, and subject to various exceptions, restricts certain business transactions between a corporation and a stockholder owning 15% or more of the corporation’s outstanding voting stock (“an interested stockholder”) for a period of three years from the date the stockholder becomes an interested stockholder.

In addition, our board of directors has adopted a stockholder rights plan. This plan would cause the substantial dilution of the holdings of any person that attempts to acquire us without the approval of our board of directors.

| Item 1B. | Unresolved Staff Comments. |

None.

15

| Item 2. | Properties. |

We do not own any real property. We lease office and warehouse space at the following locations:

| Madison Heights | MI | |

| New York | NY | |

| Bennington | VT | |

| Olathe | KS | |

| Santa Fe Springs | CA | |

| Mississauga | Ontario, Canada |

We believe that such office and warehouse space is suitable and adequate for our business.

| Item 3. | Legal Proceedings. |

We are involved in legal proceedings arising out of the ordinary course and conduct of our business, the outcomes of which are not determinable at this time. We have insurance policies covering such potential losses where such coverage is cost effective. In our opinion, any liability that might be incurred by us upon the resolution of these claims and lawsuits will not, in the aggregate, have a material adverse effect on our financial condition, results of operations or cash flows.

16

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Our common stock is currently traded on the NYSE Amex under the symbol INFU. Our warrants and units are currently traded on the OTC Bulletin Board under the symbols INHIU.OB and INHIW.OB, respectively. Prior to December 23, 2010, our common stock was traded on the OTC Bulletin Board under the symbol INHI.OB.

Each warrant entitles the holder to purchase from us one share of our common stock at an exercise price of $5.00. Our warrants will expire at 5:00 p.m., New York City time, on April 11, 2011, or earlier upon redemption.

The following tables set forth, for the calendar quarter indicated, the quarterly high and low bid information of our common stock, units and warrants, respectively, as reported on the NYSE Amex or the OTC Bulletin Board, as applicable. The quotations listed below reflect interdealer prices, without retail markup, markdown or commission and may not necessarily represent actual transactions.

Common Stock

| Quarter ended |

High | Low | ||||||

| December 31, 2010 |

$ | 2.70 | $ | 2.10 | ||||

| September 30, 2010 |

$ | 2.70 | $ | 2.05 | ||||

| June 30, 2010 |

$ | 2.70 | $ | 2.25 | ||||

| March 31, 2010 |

$ | 2.85 | $ | 2.10 | ||||

| December 31, 2009 |

$ | 3.00 | $ | 2.15 | ||||

| September 30, 2009 |

$ | 3.00 | $ | 2.15 | ||||

| June 30, 2009 |

$ | 3.25 | $ | 2.08 | ||||

| March 31, 2009 |

$ | 2.50 | $ | 1.52 | ||||

Units*

| Quarter ended |

High | Low | ||||||

| December 31, 2010 |

$ | 2.05 | $ | 2.05 | ||||

| September 30, 2010 |

$ | 1.50 | $ | 1.50 | ||||

| June 30, 2010 |

$ | 1.50 | $ | 1.50 | ||||

| March 31, 2010 |

$ | 2.45 | $ | 2.35 | ||||

| December 31, 2009 |

$ | 2.20 | $ | 2.10 | ||||

| September 30, 2009 |

$ | 2.10 | $ | 2.10 | ||||

| June 30, 2009 |

$ | 2.10 | $ | 2.10 | ||||

| March 31, 2009 |

$ | 2.10 | $ | 2.10 | ||||

| * | There are 1,650 units outstanding as of December 31, 2010 which are included within common stock in the consolidated financial statements. |

Warrants

| Quarter ended |

High | Low | ||||||

| December 31, 2010 |

$ | .04 | $ | .01 | ||||

| September 30, 2010 |

$ | .08 | $ | .02 | ||||

| June 30, 2010 |

$ | .10 | $ | .06 | ||||

| March 31, 2010 |

$ | .09 | $ | .053 | ||||

| December 31, 2009 |

$ | .10 | $ | .05 | ||||

| September 30, 2009 |

$ | .11 | $ | .05 | ||||

| June 30, 2009 |

$ | .12 | $ | .065 | ||||

| March 31, 2009 |

$ | .125 | $ | .05 | ||||

17

Holders of Common Equity

As of February 16, 2011, we had approximately 359 stockholders of record of our common stock. This does not include beneficial owners of our common stock, including Cede & Co., nominee of the Depository Trust Company.

Dividends

We have not paid any dividends on our common stock to date. The payment of dividends in the future will be contingent upon our revenues and earnings, if any, capital requirements and general financial condition. Under the terms of our credit agreement with Bank of America, N.A. and KeyBank National Association, we are not permitted to pay dividends. It is the present intention of our board of directors to retain all earnings, if any, for use in our business operations and, accordingly, our board of directors does not anticipate declaring any dividends in the foreseeable future.

Equity Compensation Plan Information

The following table provides information as of December 31, 2010 with respect to compensation plans, including individual compensation arrangements, under which our equity securities are authorized for issuance.

| Plan Category |

Number of securities to be issued upon exercise of outstanding options, warrants and rights |

Weighted-average exercise price of outstanding options, warrants and rights (2) |

Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) |

|||||||||

| (a) | (b) | (c) | ||||||||||

| Equity compensation plans approved by security holders (1) |

191,229 | $ | 2.66 | 68,437 | ||||||||

| Equity compensation plans not approved by security holders (3) |

2,112,500 | Not Applicable | Not Applicable | |||||||||

| Total |

2,303,729 | $ | 2.66 | 68,437 | ||||||||

| (1) | This amount includes 60,750 shares of common stock issuable upon the vesting of certain restricted stock awards (the “Restricted Stock Awards”) and 130,479 shares of common stock issuable upon the exercise of a vested stock option award (the “Stock Option”) made under the InfuSystem Holdings, Inc. 2007 Stock Incentive Plan (the “Plan”). This amount does not include 237,500 shares of common stock which vested under the terms of the Restricted Stock Awards during the year ended December 31, 2010. This amount also does not include 1,125,000 shares of common stock issuable upon the vesting of Restricted Stock Awards granted to directors in 2010, all of which vested prior to December 31, 2010. |

| (2) | Represents the exercise price of the Stock Option. |

| (3) | This amount includes 2,112,500 shares of common stock issuable upon the vesting of certain Restricted Stock Awards made outside of the Plan during the year ended December 31, 2010. This amount does not include 62,500 shares of common stock which vested under the terms of the Restricted Stock Awards during the year ended December 31, 2010. This amount also does not include 50,000 shares of common stock issuable upon the vesting of a Restricted Stock Award granted to a director in 2010, all of which vested prior to December 31, 2010. |

18

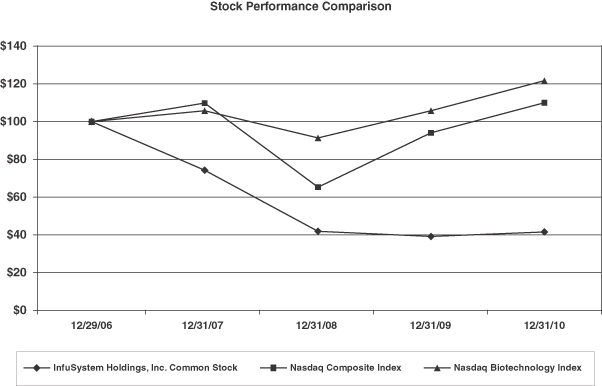

Stock Performance Graph

The graph set forth below compares the change in the our cumulative total stockholder return on our common stock between December 29, 2006 and December 31, 2010 with the cumulative total return of the NASDAQ Composite Index and the NASDAQ Biotechnology Index during the same period. This graph assumes the investment of $100 on December 29, 2006 in our common stock and each of the comparison groups and assumes reinvestment of dividends, if any. We have not paid any dividends on our common stock, and no dividends are included in the report of our performance. This graph is not “soliciting material,” is not deemed filed with the SEC and is not to be incorporated by reference in any of our filings under the Securities Act or the Exchange Act whether made before or after the date hereof and irrespective of any general incorporation language in any such filing.

| 12/29/06 | 12/31/07 | 12/31/08 | 12/31/09 | 12/31/10 | ||||||||||||||||

| InfuSystem Holdings, Inc. Common Stock |

$ | 100.00 | $ | 74.24 | $ | 42.04 | $ | 39.36 | $ | 41.68 | ||||||||||

| Nasdaq Composite Index |

$ | 100.00 | $ | 109.81 | $ | 65.29 | $ | 93.95 | $ | 109.84 | ||||||||||

| Nasdaq Biotechnology Index |

$ | 100.00 | $ | 105.71 | $ | 91.38 | $ | 105.68 | $ | 121.52 | ||||||||||

Recent Sales of Unregistered Securities

None.

Repurchases of Equity Securities

As previously announced, our board of directors has authorized a share repurchase program of up to $2 million of our outstanding common shares. The repurchase program will be funded by our available cash balance.

19

Stock repurchases may be made through open market transactions, negotiated purchases or otherwise, at times and in such amounts as our management deems to be appropriate. The timing and actual number of shares repurchased will depend on a variety of factors, including price, financing and regulatory requirements, as well as other market conditions. The program does not require us to repurchase any specific number of shares or to complete the program within a specific period of time.

The following table provides information about our purchased of common stock during the fourth quarter of the year ended December 31, 2010:

| (period) |

Total Number of Shares Purchased |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs |

Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plans or Programs |

||||||||||||

| October 1, 2010 — October 31, 2010 |

— | $ | — | — | $ | — | ||||||||||

| November 1, 2010 — November 30, 2010 |

9,574 | 2.45 | 9,574 | 1,976,000 | ||||||||||||

| December 1, 2010 — December 31, 2010 |

36,247 | 2.46 | 36,247 | 1,887,000 | ||||||||||||

| Total for fourth quarter of 2010 |

45,821 | $ | 2.46 | 45,821 | $ | 1,887,000 | ||||||||||

20

| Item 6. | Selected Financial Data. |

InfuSystem Holdings, Inc. and Subsidiaries

You should read the following selected financial data together with our financial statements and related notes included in Item 8 of this Annual Report on Form 10-K, and with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in Item 7 of this Annual Report on Form 10-K. We have derived the statement of operations data for the years ended December 31, 2010, 2009 and 2008 and the balance sheet data as of December 31, 2010 and 2009 from our audited financial statements, which are included in Item 8 of this Annual Report on Form 10-K. Our historical results for any period are not necessarily indicative of results to be expected for any future period. The information for InfuSystem Holdings, Inc. for the year ended December 31, 2007 includes operations for InfuSystem from October 26, 2007 through December 31, 2007.

Statement of Operations Data (1)

| (in thousands, except per share data) |

Year Ended December 31, 2010 |

Year Ended December 31, 2009 |

Year Ended December 31, 2008 |

Year Ended December 31, 2007 |

||||||||||||

| Net revenues |

$ | 47,229 | $ | 38,964 | $ | 35,415 | $ | 6,582 | ||||||||

| Total operating expenses |

(48,167 | ) | (33,636 | ) | (30,629 | ) | (8,079 | ) | ||||||||

| Total other (loss) income |

(2,285 | ) | (3,577 | ) | 6,080 | (189 | ) | |||||||||

| Income tax (benefit) expense |

(1,371 | ) | (977 | ) | (907 | ) | (1,110 | ) | ||||||||

| Net (loss) income |

(1,852 | ) | 774 | 9,959 | (2,796 | ) | ||||||||||

| Net (loss) income per share — basic |

$ | (0.09 | ) | $ | 0.04 | $ | 0.56 | $ | (0.15 | ) | ||||||

| Net (loss) income per share — diluted |

$ | (0.09 | ) | $ | 0.04 | $ | 0.53 | $ | (0.15 | ) | ||||||

| Balance Sheet Data (at period end) (1) | ||||||||||||||||

| (in thousands) |

December 31, 2010 |

December 31, 2009 |

December 31, 2008 |

December 31, 2007 |

||||||||||||

| Total assets |

$ | 130,364 | $ | 114,690 | $ | 116,220 | $ | 116,426 | ||||||||

| Long-term debt, including current maturities |

32,197 | 24,141 | 30,669 | 32,294 | ||||||||||||

| Stockholders’ equity |

85,086 | 81,465 | 80,073 | 68,759 | ||||||||||||

| (1) | On October 25, 2007, we completed our acquisition of 100% of the issued and outstanding capital stock of InfuSystem from I-Flow pursuant to the terms of the Stock Purchase Agreement. InfuSystem’s results of operations are included in our Consolidated Statements of Operations from the date of the acquisition. For more information, see Note 3 “Acquisitions” to our Consolidated Financial Statements which are included in this Annual Report on Form 10-K. |

Predecessor InfuSystem

The statement of operations data for the period from January 1, 2007 to October 25, 2007 and fiscal year ended December 31, 2006 and the balance sheet data as of December 31, 2006 was derived from the audited financial statements of Predecessor InfuSystem, which are not included in this report.

Statement of Operations Data

| January 1, 2007 to October 25, 2007 |

Year Ended December 31, 2006 |

|||||||

| Net revenues |

$ | 25,001 | $ | 31,716 | ||||

| Cost of revenues |

6,702 | 8,455 | ||||||

| Total operating expenses |

15,673 | 15,091 | ||||||

| Income tax expense |

1,086 | 3,094 | ||||||

| Net income |

1,777 | 4,963 | ||||||

21

Balance Sheet Data (at period end)

| December 31, 2006 |

||||

| Total assets |

$ | 27,628 | ||

| Stockholders’ equity |

22,008 | |||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

Overview

We are the leading provider of infusion pumps and related services. We service hospitals, oncology practices and other alternate site healthcare providers. Headquartered in Madison Heights, Michigan, we deliver local, field-based customer support, and also operate Centers of Excellence in Michigan, Kansas, California, and Ontario, Canada.