UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C., 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2007

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 000-51902

INFUSYSTEM HOLDINGS, INC.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 20-3341405 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

1551 East Lincoln Avenue, Suite 200

Madison Heights, Michigan 48071

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code:

(248) 546-7047

Securities Registered Pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on which Registered | |

| None | None |

Securities Registered Pursuant to 12(g) of the Act

Common Stock, par value $0.0001 per share

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter periods as the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See definition of “accelerated filer” and “large accelerated filer” in Rule 12b-2 of the Exchange Act. (check one)

| Large accelerated filer | ¨ | Accelerated filer x | ||

| Non-accelerated filer | ¨ | Smaller reporting company ¨ | ||

| (Do not check if smaller reporting company.) | ||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). YES ¨ NO x

The aggregate market value of the registrant’s voting equity held by non-affiliates of the registrant, computed by reference to the closing sales price for the registrant’s common stock on June 29, 2007, as reported on the OTC Bulletin Board, was approximately $97,707,703. In determining the market value of the voting equity held by non-affiliates, securities of the registrant beneficially owned by directors and officers of the registrant have been excluded. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares of the registrant’s common stock outstanding as of March 13, 2008 was 16,824,295.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of this registrant’s definitive proxy statement for its 2008 Annual Meeting of Stockholders to be filed with the SEC no later than 120 days after the end of the registrant’s fiscal year are incorporated herein by reference in Part III of this Annual Report on Form 10-K.

i

Cautionary Statement about Forward-Looking Statements

This Annual Report on Form 10-K includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements other than statements of historical facts contained in this Annual Report on Form 10-K, including statements regarding the future financial position, business strategy and plans and objectives of management for future operations, are forward-looking statements. The words “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “expect,” and similar expressions, as they relate to us, are intended to identify forward-looking statements. We have based these forward-looking statements largely on current expectations and projections about future events and financial trends that we believe may affect financial condition, results of operations, business strategy and financial needs. These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including, without limitation, those described in “Risk Factors” and elsewhere in this Annual Report on Form 10-K, including, among other things:

| • | dependence on our Medicare Supplier Number; |

| • | changes in third-party reimbursement rates; |

| • | availability of chemotherapy drugs used in our infusion pump systems; |

| • | physician’s acceptance of infusion pump therapy over oral medications; |

| • | growth strategy, involving entry into new fields of infusion-based therapy; |

| • | industry competition; |

| • | dependence upon our suppliers; and |

| • | compliance with U.S. GAAP. |

These risks are not exhaustive. Other sections of this Annual Report on Form 10-K include additional factors which could adversely impact our business and financial performance. Moreover, we operate in a very competitive and rapidly changing environment. New risk factors emerge from time to time and it is not possible for us to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

You should not rely upon forward looking statements as predictions of future events. We cannot assure you that the events and circumstances reflected in the forward looking statements will be achieved or occur. Although we believe that the expectations reflected in the forward looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements.

References in this Annual Report on Form 10-K to “we,” “us,” or the “Company” are to InfuSystem Holdings, Inc. and its subsidiary. From September 28, 2006 through October 25, 2007, the subsidiary was Iceland Acquisition Subsidiary, Inc. (“Iceland Acquisition Subsidiary”). As of October 25, 2007, the subsidiary was InfuSystem, Inc. (“InfuSystem”).

| Item 1. | Business. |

Background

We were formed as a Delaware blank check company in 2005 for the purpose of acquiring through a merger, capital stock exchange, asset acquisition or other similar business combination, one or more operating businesses in the healthcare sector. We completed our initial public offering on April 18, 2006. On September 29, 2006, we entered into a Stock Purchase Agreement (as, amended the “Stock Purchase Agreement”) with I-Flow Corporation (“I-Flow”), Iceland Acquisition Subsidiary, our wholly-owned subsidiary, and InfuSystem, a wholly-owned subsidiary of I-Flow Corporation. Upon the closing of the transactions contemplated by the Stock Purchase Agreement on October 25, 2007, Iceland Acquisition Subsidiary purchased all of the issued and outstanding capital stock of InfuSystem from I-Flow and concurrently merged with and into InfuSystem. As a result of the merger, Iceland Acquisition Subsidiary ceased to exist as an independent entity and InfuSystem, as the corporation surviving the merger, became our wholly-owned subsidiary. Effective October 25, 2007, we changed our corporate name from “HAPC, INC.” to InfuSystem Holdings, Inc.

InfuSystem was incorporated under the laws of the State of California in December 1997 under the name I-Flow Subsidiary, Inc., as a wholly owned subsidiary of I-Flow. In February 1998, I-Flow Subsidiary, Inc. acquired Venture Medical, Inc. and InfuSystem II, Inc. in a merger transaction pursuant to which I-Flow Subsidiary, Inc. as the surviving corporation changed its name to InfuSystem, Inc.

Business Concept and Strategy

We are a provider of ambulatory infusion pump management services for oncologists in the United States. Ambulatory infusion pumps are small, lightweight electronic pumps designed to be worn by patients in their homes which allow patients the freedom to move about while receiving chemotherapy treatments. The pumps are battery powered and attached to intravenous administration tubing, which is in turn attached to a bag or plastic cassette that contains the chemotherapy drug.

Our business model is currently highly focused on oncology chemotherapy infusion. To our knowledge, we are the only national ambulatory infusion pump service provider focused on oncology.

We supply electronic ambulatory infusion pumps and associated disposable supply kits to physicians’ offices, infusion clinics and hospital outpatient chemotherapy clinics to be utilized by patients who receive continuous chemotherapy infusions. We obtain an assignment of insurance benefits from the patient, bill the insurance company or patient accordingly, and collect payment. We provide pump management services for the pumps and associated disposable supply kits to approximately 1,550 oncology practices in the United States. We retain title to the pumps during this process. In addition, we sell safety devices for cytotoxic drug transfer and administration and we rent pole-mounted or ambulatory infusion pumps for use within the oncology practice.

We purchase electronic ambulatory infusion pumps from a variety of suppliers on a non-exclusive basis. Such pumps are generic in nature and are available to our competitors. The pumps are currently used primarily for continuous infusion of chemotherapy drugs for patients with colorectal cancer.

One aspect of our business strategy over the next one to three years is to expand into treatment of other cancers such as head, neck and gastric. In addition to treatments for colorectal cancer, there are a number of other drugs currently approved by the U.S. Food and Drug Administration (the “FDA”), as well as agents in the pharmaceutical development pipeline, which we believe could potentially be used with continuous infusion

2

protocols for the treatment of other diseases. These approved drugs and drugs in the pharmaceutical development pipeline include the following: Gemcitabine, Idarubicin and Topotecan. We currently generate approximately 15% of our revenue from treatments for disease states other than colorectal cancer. Drugs or protocols currently in clinical trials may also obtain regulatory approval over the next several years. If these new drugs obtain regulatory approval for use with continuous infusion protocols, we expect the pharmaceutical companies to focus their sales and marketing forces on promoting the new drugs and protocols to physicians.

Another aspect of our business strategy over the next one to three years is to actively pursue opportunities for expansion through acquisitions, joint ventures and strategic alliances. We believe there are numerous opportunities to acquire smaller, regional competitors that perform similar services to us, but do not have the national presence, network of managed care contracts or economies of scale that we currently enjoy. We believe that the successful integration of these businesses into our operations will potentially enable us to achieve higher profit margins from them than they could achieve operating independently.

We face risks that other competitors can provide the same services as us. Those risks are currently mitigated by our existing managed care contracts and economies of scale, which allow for less costly purchase and management of the pumps. Additionally, we have already established a long standing relationship as a provider of pumps to approximately 1,550 oncology practices in the United States. We believe that there are competitive barriers to entry against other suppliers with respect to these oncology practices because we have an established national presence and managed care contracts in place covering over 125,000,000 managed care lives, (i.e. persons enrolled in various managed care plans or commercial insurance carriers such as health maintenance organizations and preferred provider organizations) increasing the likelihood that we participate in the insurance networks of patients to whom physicians wish to refer to an ambulatory infusion pump provider. Moreover, we have an available inventory of approximately 17,000 active ambulatory infusion pumps, which may allow us to be more responsive to the needs of physicians and patients than a new market entrant. We do not perform any research and development.

Continuous Infusion Therapy

Continuous infusion of chemotherapy involves the gradual administration of a drug via a small, lightweight, portable electronic infusion pump over a prolonged period of time, defined as greater than 8 hours, and up to 24 hours daily. A cancer patient can receive his or her medicine on average 5 to 30 days a month depending on the chemotherapy regimen that is most appropriate to that individual’s health status and disease process. This may be followed by periods of rest and then repeated cycles with treatment goals of progression free disease survival. This drug administration method has replaced “bolus” administration in specific circumstances. The advantages of slow continuous low doses of specific drugs are well documented. Clinical studies support use of continuous infusion chemotherapy for decreased toxicity without loss of anti-tumor efficacy while emerging evidence shows improved drug activity. The 2007/2008 National Comprehensive Cancer Network Guidelines recommend the use of continuous infusion for treatment of numerous cancer diagnoses. We believe that the growth of continuous infusion therapy is driven by three factors: superior clinical outcomes; enhanced patient response and convenience; and recent changes to physician reimbursement.

| • | In the past decade, significant progress has been made in the treatment of colorectal cancer due to advances in surgery, radiotherapy and chemotherapy. The survival benefit of 5-Fluorouracil based chemotherapy for patients with Stage III colorectal cancer has been established during this time. In the late 1990s, overwhelming evidence revealed that the delivery method of the drug (or schedule) was key to drug availability, efficacy and tolerability. Schedule dependant anti-tumor activity and toxicity has resulted in continuous infusion 5-Fluorouracil being adopted as standard of care. In 2000, the FDA approved Camptosar (the trade name for the generic chemotherapy drug Irinotecan), a drug developed by Pfizer, for first-line therapy in combination with 5-Fluorouracil for the treatment of colorectal cancer. In 2002, the FDA approved Eloxatin (the trade name for the generic chemotherapy drug Oxaliplatin), a drug developed by Sanofi-Aventis, for use in combination with continuous infusion 5-Fluorouracil for the treatment of colorectal cancer. FOLFIRI, the chemotherapy protocol which includes Camptosar in combination with continuous infusion 5-Fluorouracil and the drug Leucovorin, and FOLFOX, the chemotherapy protocol which includes Eloxatin, in combination with continuous infusion 5-Fluorouracil and the Leucovorin, have resulted in significantly improved overall |

3

| survival rates for colorectal cancer patients at various stages of the disease state. Sanofi-Aventis and Pfizer are each dedicating significant resources to educate physicians and promote the use of FOLFOX and FOLFIRI. Oncologists have responded and the adoption of continuous infusion treatments has steadily grown for colorectal cancer. |

| • | The use of continuous infusion has been demonstrated to decrease or alter the toxicity of a number of cytotoxic, or cell killing agents. Higher doses of drugs can be infused over longer periods of time, leading to improved tolerance and decreased toxicity. For example, the cardiotoxicity (heart muscle damage) of the chemotherapy drug Doxorubicin is decreased by schedules of administration (The Chemotherapy Source Book, Perry, M.C., 2008). Nausea, vomiting, diarrhea and decreased white blood cell and platelet counts are all affected by duration of delivery. Continuous infusion can lead to improved tolerance and patient comfort while enhancing the patient’s ability to remain on the chemotherapy regimen. |

| • | Continuous infusion offers convenience to the cancer patient. Fatigue, a prevalent side-effect of cancer treatment, is compounded by repeated day-long treatments at the physician’s office. Ambulatory pump use for drug therapy allows the patient to complete treatment while attending to activities of daily living or relaxing in his or her own home. Physician administration of the pump provides for continuity of care. The partnering of physician management and patient autonomy provide for the highest quality of care with the greatest patient satisfaction. |

| • | The Medicare Modernization Act of 2003 reduced levels of Medicare reimbursement for oncology drugs administered in the physician office setting. To offset this reduction, Medicare increased the service fees paid to oncologists. We believe that this has resulted in doctors shifting to treatments that provide superior efficacy and patient satisfaction while optimizing their potential to earn service fees. |

Products and Services

Our core service is to provide oncology offices, infusion clinics and hospital out-patient chemotherapy clinics with ambulatory infusion pumps in addition to related supplies for patient use, and then directly bill and collect payment from payors and patients for the use of these pumps. We own approximately 17,000 pumps. At any given time, it is estimated that approximately 60% of the pumps are in the possession of patients. The remainder of the pumps is in transport for cleaning, calibration or as back-ups.

After a doctor determines that a patient is eligible for ambulatory infusion pump therapy, the doctor arranges for the patient to receive an infusion pump and provides the necessary chemotherapy drugs. The oncologist and nursing staff train the patient in the use of the pump and initiate service. The physician bills insurers, Medicare, Medicaid, managed care companies or patients (collectively, “payors”) for the physician’s professional services associated with initiating and supervising the infusion pump administration, as well as the supply of drugs. We directly bill payors for the use of the pump and related disposable supplies. We have contracts with more than 100 payors that cover more than 125 million managed care lives. Billing to payors requires coordination with patients and physicians who initiate the service, as physicians’ offices must provide us with appropriate paperwork (patient’s insurance information, certificate of medical necessity and an acknowledgement of benefits that shows receipt of equipment by the patient) in order for us to bill the payors.

In addition to providing high quality and convenient care, we believe that our pump management program offers significant economic benefits for patients, providers and payors.

| • | We benefit patients by providing high quality, reliable pumps and accessories as well as 24-hour service and support. We employ oncology and intravenous certified registered nurses trained on ambulatory infusion pump equipment who staff our 24-hour hotline to address questions that patients may have about their pump treatment, the infusion pumps or other medical or technical questions related to the pumps. |

4

| • | Physicians benefit from our service in several ways. For those physicians wishing to provide pumps to their patients, by utilizing our model, we can relieve such physicians of the capital commitment, pump service, maintenance and billing and administrative burdens associated with pump ownership. Rather than referring patients to home care, our service allows the doctor to continue a direct relationship with the patient and to receive professional service fees for setting up treatment and administering drugs. We provide physicians the pumps and related administration sets and accessories while retaining title to the pumps. We directly bill the patients’ insurance companies for the use of the pumps. As there is no purchase on the part of the physician, there is no capital commitment. We bill insurance providers for the technical component (pump usage and related supplies) and the physician bills insurance providers for the related professional services. |

| • | Payors support us because our service is generally less expensive than hospitalization or home care. |

Relationships with Physician Offices

Through our direct sales force, we maintain relationships with clinical oncologists in more than 1,550 practices. Though this represents a substantial portion of the oncologists in the United States, we believe we can continue to expand our network to further penetrate the oncology market. Over the past three years, we have added approximately 425 new accounts to our services. We believe our relationships with physician offices are strong, as evidenced by our significant retention rate (98.5% of the physician offices serviced during fiscal year 2006 remained customers during fiscal year 2007).

We believe that, in general, we do not compete directly with hospitals and physician offices to treat patients. Rather, by providing products and services to hospitals and physician offices and other care facilities and providers, we believe that we can help providers keep up with increasing patient demand and manage institutional constraints on capital and manpower due to the nature of limited resources in hospitals and physician offices.

Billing Collection Services

Prior to our acquisition of InfuSystem, InfuSystem had been providing billing and collection services to I-Flow for its ON-Q® product. On October 25, 2007, InfuSystem and I-Flow entered into an Amended and Restated Services Agreement (the “Services Agreement”) pursuant to which InfuSystem agreed to continue to provide I-Flow with these services. The initial term of the Services Agreement is three years. The Services Agreement will automatically be renewed for succeeding one year terms unless terminated pursuant to certain cancellation provisions. I-Flow has agreed to pay InfuSystem a monthly service fee equal to the greater of (i) the monthly expenses for those InfuSystem employees devoted to the billing and collection and management services provided to I-Flow which expenses shall consist of (a) salaries and wages, (b) payroll taxes and (c) group insurance, in addition to an amount equal to 40% of the sums of items (a) through (c) or (ii) a performance-based fee equal to 25% of the total actual net cash collections (net of adjustments) received during such month on behalf of I-Flow. InfuSystem currently maintains a staff of 9 people to provide billing and collection services to I-Flow.

In order to facilitate the continued business relationship between InfuSystem and I-Flow under the Services Agreement, described above, InfuSystem and I-Flow entered into a license agreement on October 25, 2007 (the “License Agreement”) pursuant to which InfuSystem granted I-Flow a license to use InfuSystem’s intellectual property related to the third-party billing and collection services and management services provided by InfuSystem to I-Flow. Specifically, InfuSystem granted I-Flow (i) an unrestricted, perpetual, irrevocable, worldwide, assignable, royalty-free and exclusive license to use and/or sublicense InfuSystem’s intellectual property with respect to acute post-operative pain management treatments, and (ii) an unrestricted, perpetual, irrevocable, worldwide, assignable, royalty-free and non-exclusive license to use and/or sublicense InfuSystem’s intellectual property with respect to all fields other than post-operative pain management treatments, including, without limitation, the fields of wound site management and post-operative surgical treatments.

5

The term of the License Agreement is perpetual, but may be terminated by I-Flow following the third anniversary of the effective date of the License Agreement. Upon the later of the third anniversary of the effective date or the termination of the Services Agreement for any reason, the exclusive license will be deemed amended to become a non-exclusive license. InfuSystem may not terminate the License Agreement.

On November 8, 2007, I-Flow informed InfuSystem that it was terminating the Services Agreement effective May 10, 2008. I-Flow’s license to use and/or sublicense InfuSystem’s intellectual property with respect to acute post-operative pain management treatments will thereafter become non-exclusive. During 2007, we recorded revenues of $103,000 from this arrangement, which are included in net revenues.

Employees

As of December 31, 2007, we had 107 employees, including 100 full-time employees and 7 part-time employees. None of our employees are unionized.

Material Suppliers

We supply a wide variety of pumps and associated equipment, as well as disposables and ancillary supplies. The majority of our pumps are electronic ambulatory pumps purchased from the following manufacturers, each of which is material and supplies more than 10% of the pumps purchased by us: Smiths Medical, Inc.; Hospira Worldwide, Inc.; and McKinley Medical, LLC. There are no supply agreements in place with any of the suppliers. All purchases are handled pursuant to pricing agreements, which contain no material terms other than prices that are subject to change by the manufacturer. As of December 31, 2007, we owned approximately 17,000 active pumps.

Seasonality

We do not believe that there is significant seasonality of our business.

Environmental Laws

We are required to comply with applicable environmental laws regulating the disposal of cleaning agents used in the process of cleaning our ambulatory infusion pumps, as well as the disposal of sharps and blood products used in connection with the pumps. We do not believe that compliance with such laws has a material effect on our business.

Significant Customers

We have sought to establish contracts with as many managed care organizations as commercially practicable, in an effort to ensure that reimbursement is not a significant obstacle for providers who recommend continuous infusion therapy and wish to utilize our services. A managed care organization is a health care payor (or a group of medical services payors) that contracts to provide a wide variety of healthcare services to enrolled members through participating providers (such as us). A payor is any entity that pays on behalf of a member patient.

We currently have contracts with more than 100 managed care plans that cover approximately 125 million lives. Material terms of contracts with managed care organizations are typically a set fee or rate, or discount from billed charges for equipment provided. These contracts generally provide for a term of one year, with automatic one-year renewals, unless we or the contracted payor do not wish to renew. Contracted payors include managed care organizations, Medicare, commercial Medicare replacement plans, Blue Cross/Blue Shield plans, self-insured plans and numerous other commercial insurance carriers.

Through December 31, 2007, we experienced increased collection delays from non-contracted Blue Cross/Blue Shield affiliates. This was primarily due to the fact that all of our non-contracted billings were submitted to Blue Cross of Michigan (“BCBSM”) through the national BlueCard program. BCBSM processes our hard copy claims and generates electronic files to out of state Blue Cross plans under which the patients’ policies are carried. This results in a very slow payment process and a high volume of claim rejections requiring additional information. We are working with BCBSM personnel to rectify this issue.

6

Competitors

We believe that our competition is primarily composed of regional providers, hospital-owned durable medical equipment (“DME”) providers, physician providers and home care infusion providers. An estimate of the number of competitors is not known or reasonably available, due to the wide variety in type and size of the market participants described below. We are not aware of any industry reports with respect to the competitive market described below. The description of market segments and business activities within those market segments is based on our experiences in the industry.

| • | Regional Providers: Regional DME providers act as distributors for a variety of medical products. We believe regional DME provider sales forces generally consist of a relatively small number of salespeople, usually covering one or two states in total. Regional DME providers tend to carry a limited selection of infusion pumps and their salespeople generally have limited resources. Regional DME providers usually do not have 24-hour nursing service. InfuSystem believes that regional DME providers have relatively few managed care contracts, which may prevent these providers from being paid at acceptable levels and may also result in higher out-of-pocket costs for patients. |

| • | Hospital—Owned DME Providers: Many hospitals have in-house DME providers to supply basic equipment. In general, however, these providers have limited capital and tend to stock a small inventory of infusion pumps. As a result, InfuSystem believes that hospital-owned providers have limited ability to grow because of restricted patient populations. Growth from outside of the hospital may pose a challenge because hospitals typically will not provide referrals to competitors, instead preferring to offer patients a choice of non-hospital-affiliated DME providers. |

| • | Physician Providers: A limited number of physicians maintain an inventory of their own infusion pumps and collect both the professional and technical fees. However, we believe that pump utilization in this area tends to be low and the costs associated with ongoing supplies, preventative maintenance and repairs can be relatively high. Moreover, we believe that a high percentage of DME claims are rejected by payors upon first submission, requiring a provider’s staff to spend significant time and effort to resubmit claims and receive payment for treatment. The numerous service and technical questions from patients may present another significant cost to a physician provider’s staff. |

| • | Home Care Infusion Providers: Home care infusion providers provide chemotherapy drugs and services to allow for in-home patient treatment. Although the doctor is still responsible for overseeing the treatment and assuming the liability for the patient’s treatment and outcome, we believe that the physician is often not reimbursed for this ongoing responsibility. Moreover, we believe that home care infusion treatment can be very costly and that many patients do not carry this type of insurance coverage, resulting in larger out-of-pocket costs. Because home care treatments may take as long as six months, these costs can be high and can result in higher patient co-payments. We believe that home care providers may also be reluctant to offer 24-hour coverage or additional patient visits, due to capped fees. |

Regulation of Our Business

Our business is subject to certain regulations. Specifically, as a Medicare supplier of DME and related supplies, we must comply with the rules (the “DMEPOS Supplier Standards”) established by the Health Care Financing Administration regulating Medicare suppliers of DME and prosthetics, orthotics and supplies (“DMEPOS”). The DMEPOS Supplier Standards consist of 21 requirements that must be met in order for a DMEPOS supplier to be eligible to receive payment for a Medicare-covered item. The most significant DMEPOS Supplier Standards require us to (i) advise Medicare beneficiaries of their option to purchase certain equipment, (ii) honor all warranties under state law and not charge Medicare beneficiaries for the repair or replacement of equipment or for services covered under warranty, (iii) permit agents of the Centers for Medicare and Medicaid Services to conduct on-site inspections to ascertain compliance with the DMEPOS Supplier Standards, (iv) maintain

7

liability insurance, (v) refrain from contacting Medicare beneficiaries by telephone, except in certain limited circumstances, (vi) answer questions and respond to complaints of beneficiaries regarding the supplied equipment, (vii) disclose the DMEPOS Supplier Standards to each Medicare beneficiary to whom it supplies equipment and (viii) maintain a complaint resolution procedure and record certain information regarding each complaint.

We are also subject to the provisions of the Health Insurance Portability and Accountability Act of 1996 (“HIPAA”) designed to protect the security and confidentiality of certain patient health information. Under HIPAA, we must provide patients with access to certain records and must notify patients of our use of personal medical information and patient privacy rights. Moreover, HIPAA sets limits on how we may use individually identifiable health information and prohibits the use of patient information for marketing purposes.

Available Information

Our Internet address is www.infusystem.com. On this Web site, we post the following filings as soon as reasonably practicable after they are electronically filed with or furnished to the U.S. Securities and Exchange Commission (the “SEC”): our Annual Report on Form 10-K; our Quarterly Reports on Form 10-Q; our Current Reports on Form 8-K; our proxy statement related to our annual stockholders’ meeting; and any amendments to those reports or statements. All such filings are available on our Web site free of charge. The content on our Web site is not incorporated by reference into this Annual Report on Form 10-K unless expressly noted.

| Item 1A. | Risk Factors. |

An investment in our securities involves a high degree of risk. You should consider carefully all of the material risks described below, together with the other information contained in this Annual Report on Form 10-K. If any of the following events occur, our business, financial conditions and results of operations may be materially adversely affected.

RISK FACTORS RELATING TO OUR BUSINESS AND THE INDUSTRY IN WHICH WE OPERATE.

We are dependent on our Medicare Supplier Number.

We have obtained a Medicare Supplier Number and are required to comply with Medicare Supplier Standards in order to maintain such number. If we are unable to comply with the relevant standards, we could lose our Medicare Supplier Number, which is the primary identification number used with our various third-party payors. The loss of such identification number for any reason would prevent us from billing Medicare for patients who rely on Medicare to pay their medical expenses and, as a result, we would experience a decrease in our revenues. Furthermore, all managed care and Medicaid contracts require us to have a Medicare Supplier Number. Without such a number, we would be unable to continue our managed care and Medicaid contracts and would experience a material decrease in revenues as a result. The majority of our revenue is dependent upon our Medicare Supplier Number.

Changes in third-party reimbursement rates may adversely impact our revenues.

We depend primarily on third-party reimbursement for the collection of our revenues. We are paid directly by private insurers and governmental agencies, often on a fixed fee basis, for infusion equipment and related disposable supplies provided to patients. If the average fees allowable by private insurers or governmental agencies were reduced, the negative impact on revenues could have a material adverse effect on our financial condition, results of operations and cash flows. Also, if collection amounts owed to us by patients and insurers is reduced, we may be required to increase our bad debt expense and/or decrease our revenues.

8

Our customers frequently receive reimbursement from private insurers and governmental agencies. Any change in the overall reimbursement system may adversely impact our business. The health care reimbursement system is in a constant state of change.

Changes often create financial incentives and disincentives that encourage or discourage the use of a particular type of product, therapy or clinical procedure. Market acceptance of infusion therapy may be adversely affected by changes or trends within the reimbursement system. Changes to the health care system that favor technologies or treatment regimens other than InfuSystem’s or that reduce reimbursements to providers or treatment facilities that use InfuSystem’s products may adversely affect InfuSystem’s ability to market its products profitably.

Our customers are heavily dependent on payment for their services by private insurers and governmental agencies. Changes in the reimbursement system could adversely affect our participation in the industry. We believe that the current trend in the insurance industry (both private and governmental) has been to eliminate cost-based reimbursement and to move towards fixed or limited fees for service, thereby encouraging health care providers to use the lowest cost method of delivering medications. Furthermore, certain payors may transition to competitive bidding programs to lower costs even more. These trends may discourage the use of our products, create downward pressure on our average prices, and, ultimately, negatively affect our revenues and profit margins.

Our success is impacted by the availability of the chemotherapy drugs that are used in our infusion pump systems.

We primarily derive our revenue from the rental of ambulatory infusion pump systems to oncology patients through physicians’ offices and chemotherapy clinics. A shortage in the availability of chemotherapy drugs that are used in the infusion pump systems, including the commonly-used chemotherapy drug known as 5-Fluorouracil, could have a material adverse effect on InfuSystem’s financial condition, results of operations and cash flows. For instance, we believe that a shortage of 5-Fluorouracil in the fourth quarter of 2005 resulted in an unfavorable revenue impact in excess of $1,000,000. The 5-Fluorouracil shortage continued into the first quarter of 2006 and, although availability of 5-Fluorouracil returned to normal at the end of the first quarter of 2006, revenue was affected during the second quarter of 2006 due to a decline in the number of patients in the pipeline who had to turn to other medications. Future shortages of 5-Fluorouracil or other commonly-used chemotherapy drugs could negatively impact InfuSystem’s revenue, financial condition and cash flows.

Our revenues are heavily dependent on physicians’ acceptance of infusion therapy as a preferred therapy since a significant percentage of patients are treated with oral medications. If new oral medications are introduced or future clinical studies demonstrate that oral medications are as effective or more effective than infusion therapy, our business could be adversely affected.

Continuous infusion therapy is currently preferred by many physicians over oral medication treatment despite the more cumbersome aspects of maintaining a continuous infusion regimen. The reasons for these physicians’ preference are varied, including a belief that infusion therapy involves fewer adverse side effects, reduces compliance issues and may provide greater therapeutic benefits. Numerous clinical trials are currently ongoing, evaluating and comparing the therapeutic benefits of current infusion-based regimens with various oral medication regimens. If these clinical trials demonstrate that oral medications provide equal or greater therapeutic benefits and/or demonstrate reduced side effects from prior oral medication regimens, our revenues and overall business could be materially and adversely affected. Additionally, if new oral medications are introduced to the market that are superior to existing oral therapies, physicians’ willingness to prescribe infusion-based regimens could decline, which would adversely affect our financial condition, results of operations and cash flows.

We operate our business in all 50 states of the United States and we are subject to each state’s licensure laws as a DME supplier. State licensure laws for DME suppliers are subject to change and if we fail to comply with any state’s laws, we will be unable to operate as a DME supplier in such state and our business operations will be adversely affected.

As a DME supplier operating in all 50 states of the United States, we are subject to each state’s licensure laws regulating DME suppliers. State licensure laws for DME suppliers are subject to change and we must ensure that we are continually in compliance with the laws of all 50 states. In the event that we fail to comply with any

9

state’s laws governing the licensing of DME suppliers, we will be unable to operate as a DME supplier in such state until we regain compliance. We may also be subject to certain fines and/or penalties and our business operations will be adversely affected.

Our growth strategy includes expansion into infusion treatment for cancers other than the colorectal type. There can be no assurance that infusion-based regimens for these other cancers will become accepted or that we will be successful in penetrating these different markets.

An aspect of our growth strategy is to expand into the treatment of other cancers, such as head, neck and gastric. Currently, however, there is not widespread acceptance of infusion-based therapies in the treatment of these other cancers and future acceptance of continuous infusion therapies depends on new protocols for existing drugs and approval of new drugs currently in clinical trials. No assurances can be given that these new drugs will be approved or will prove superior to oral medication or other treatment alternatives. In addition, no assurances can be given that we will be able to successfully penetrate any new markets that may develop in the future or manage the growth in additional resources that would be required.

The industry in which we operate is intensely competitive and changes rapidly. If we are unable to successfully compete with our competitors, our business operations may suffer.

The drug infusion industry is highly competitive. We compete in this industry based primarily on price, service and performance. Some of our competitors and potential competitors have significantly greater resources than we do for research and development, marketing and sales. As a result, they may be better able to compete for market share, even in areas in which our services may be superior. The industry is subject to technological changes and such changes may put our current fleet of pumps at a competitive disadvantage. If we are unable to effectively compete in our market, our financial condition, results of operations and cash flows may materially suffer.

We rely on independent suppliers for our products. Any delay or disruption in the supply of products, particularly our supply of electronic ambulatory pumps, may negatively impact our operations.

Our infusion pumps are obtained from outside vendors. The majority of our pumps are electronic ambulatory pumps which are supplied to us by three major suppliers: Smiths Medical, Inc.; Hospira Worldwide, Inc.; and McKinley Medical, LLC. The loss or breakdown of our relationships with even one of these outside vendors could subject us to substantial delays in the delivery of our products to customers. Significant delays in the delivery of products could result in possible cancellation of orders and the loss of customers. Our inability to provide products to meet delivery schedules could have a material adverse effect on our reputation in the industry, as well as our financial condition, results of operations and cash flows.

Although we do not manufacture the products we distribute, if one of the products distributed by us proves to be defective or is misused by a health care practitioner or patient, we may be subject to liability that could adversely affect our financial condition and results of operations.

Although we do not manufacture the products that we distribute, a defect in the design or manufacture of one of the products distributed by us, or a failure of products distributed by us to perform for the use specified, could have a material adverse effect on our reputation in the industry and subject us to claims of liability for injuries and otherwise. Misuse of products distributed by us by a practitioner or patient that results in injury could similarly subject us to liability. Any substantial underinsured loss could have a material adverse effect on our financial condition, results of operations and cash flows. Furthermore, any impairment of our reputation could have a material adverse effect on our revenues and prospects for future business.

The preparation of our financial statements in accordance with accounting principles generally accepted in the United States requires us to make estimates, judgments, and assumptions that may ultimately prove to be incorrect.

The accounting estimates and judgments that management must make in the ordinary course of business affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts

10

of revenue and expenses during the periods presented. If the underlying estimates are ultimately proven to be incorrect, subsequent adjustments resulting from errors could have a material adverse effect on our operating results for the period or periods in which the change is identified. Additionally, subsequent adjustments from errors could require us to restate our financial statements. Restating financial statements could result in a material decline in the price of our stock.

RISK FACTORS RELATING SPECIFICALLY TO OUR COMMON STOCK AND WARRANTS

The market price of our common stock and warrants has been, and is likely to remain volatile and may decline in value.

The market price of our common stock and warrants has been and is likely to continue to be volatile. Market prices for securities of medical device companies, including ours, have historically been volatile, and the market has from time to time experienced significant price and volume fluctuations that appear unrelated to the operating performance of particular companies. The following factors, among others, can have a significant effect on the market price of our securities:

| • | announcements of technological innovations, new products, or clinical studies by others; |

| • | government regulation; |

| • | changes in the coverage or reimbursement rates of private insurers and governmental agencies; |

| • | developments in patent or other proprietary rights; |

| • | changes in economic conditions in the United States or globally; and |

| • | comments by securities analysts and general market conditions. |

The realization of any risks described in these “Risk Factors” could also have a negative effect on the market price of our common stock and warrants.

We do not pay dividends and this may negatively affect the price of our stock.

We have not paid dividends on our common stock and do not anticipate paying dividends on our common stock in the foreseeable future. The future price of our common stock may be adversely impacted because we do not pay dividends.

Holders of our warrants may not be able to exercise the warrants if we do not maintain an effective registration statement and current prospectus covering the shares of common stock underlying the warrants.

If we do not maintain an effective registration statement and a current prospectus covering the shares of common stock issuable upon exercise of our outstanding warrants or comply with applicable state securities laws, holders of our warrants may not be able to exercise the warrants issued by us. In order for holders of our warrants to be able to exercise the warrants, the shares of common stock underlying the warrants must be covered by an effective registration statement and a current prospectus or be qualified for sale or exempt from qualification under the applicable securities laws of the state in which the warrant holder resides. Although we cannot assure holders of our warrants that we will actually be able to do so, we will use our best efforts to maintain an effective registration statement and a current prospectus covering the shares of our common stock underlying the outstanding warrants at all times when the market price of the common stock exceeds the exercise price of the warrants until the expiration of the warrants.

Future sales of our common stock may depress our stock price.

The market price of our common stock could decline as a result of sales of substantial amounts of our

11

common stock in the public market, or the perception that these sales could occur. In addition to the shares of our common stock currently available for sale in the public market, shares of our common stock sold in past private placements (which include shares held by certain members of our board of directors) and the shares of common stock underlying our outstanding warrants are subject to registration rights. If the holders of these securities choose to exercise their registration rights, this would result in an increase in the number of shares our common stock available for resale in the public market, which in turn could lead to a decrease in our stock price and a dilution of stockholders’ ownership interests. These factors could also make it more difficult for us to raise funds through future equity offerings. As of March 13, 2008 we had 16,824,295 shares of our common stock outstanding not including the 35,108,219 shares of common stock underlying our outstanding warrants.

| Item 1B. | Unresolved Staff Comments. |

Not applicable.

| Item 2. | Properties. |

We do not own any real property. We lease office and warehouse space at 1551 E. Lincoln Avenue, Madison Heights, Michigan. We believe that such office and warehouse space is suitable and adequate for our business.

| Item 3. | Legal Proceedings. |

We are involved in legal proceedings arising out of the ordinary course and conduct of our business, the outcomes of which are not determinable at this time. We have insurance policies covering such potential losses where such coverage is cost effective. In our opinion, any liability that might be incurred by us upon the resolution of these claims and lawsuits will not, in the aggregate, have a material adverse effect on our financial condition or results of operations.

| Item 4. | Submission of Matters to a Vote of Security Holders. |

We held our Special Annual Meeting of Stockholders on October 24, 2007. Each of the proposals set forth below was approved by our stockholders at the Special Annual Meeting.

Our acquisition of all of the issued and outstanding capital stock of InfuSystem pursuant to the Stock Purchase Agreement dated as of September 29, 2006, by and among us, Iceland Acquisition Subsidiary, I-Flow and InfuSystem was approved by the vote set forth below.

| Votes | ||

| For |

13,945,464 | |

| Against |

3,181,118 | |

| Abstain |

666,667 |

The amendment of our Amended and Restated Certificate of Incorporation to change our name from “HAPC, INC.” to “InfuSystem Holdings, Inc.” was approved by the vote set forth below.

| Votes | ||

| For |

15,282,735 | |

| Against |

931,747 | |

| Abstain |

1,895,000 |

The adoption of our 2007 Stock Incentive Plan was approved by the vote set forth below.

| Votes | ||

| For |

12,924,094 | |

| Against |

2,906,436 | |

| Abstain |

1,895,000 |

12

The following nominees were elected to serve as members of our board of directors, each to hold office until his successor is duly elected and qualified, by the vote set forth below:

| Nominee |

For | Withhold Authority | ||

| Sean McDevitt |

15,409,463 | 2,701,016 | ||

| John Voris |

15,411,828 | 2,698,651 | ||

| Pat LaVecchia |

15,411,828 | 2,698,651 | ||

| Wayne Yetter |

15,411,828 | 2,698,651 | ||

| Jean Pierre Millon |

15,411,828 | 2,698,651 |

Each of the foregoing individuals served as members of our board of directors immediately prior to the Special Annual Meeting of Stockholders.

The ratification of the appointment of Deloitte & Touche LLP as our registered public accounting firm for the fiscal year ended December 31, 2007 was approved by the vote set forth below.

| Votes | ||

| For |

15,289,011 | |

| Against |

886,968 | |

| Abstain |

1,934,500 |

13

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Our common stock, warrants and units currently traded on the OTC Bulletin Board under the symbols INHI.OB, INHIW.OB and INHIU.OB, respectively. Prior to January 14, 2008, our common stock, warrants and units were traded on the OTC Bulletin Board under the symbols HAPN.OB, HAPNW.OB and HANPU.OB, respectively.

Each warrant entitles the holder to purchase from us one share of our common stock at an exercise price of $5.00. Our warrants will expire at 5:00 p.m., New York City time, on April 11, 2011, or earlier upon redemption.

The following tables set forth, for the calendar quarter indicated, the quarterly high and low bid information of our units, common stock and warrants, respectively, as reported on the OTC Bulletin Board. The quotations listed below reflect interdealer prices, without retail markup, markdown or commission and may not necessarily represent actual transactions.

Units

| Quarter ended |

High | Low | ||||

| December 31, 2007 |

$ | 6.44 | $ | 3.65 | ||

| September 30, 2007 |

$ | 6.40 | $ | 6.00 | ||

| June 30, 2007 |

$ | 6.55 | $ | 6.05 | ||

| March 30, 2007 |

$ | 6.25 | $ | 6.00 | ||

| December 31, 2006 |

$ | 6.15 | $ | 5.76 | ||

| September 30, 2006 |

$ | 6.08 | $ | 5.90 | ||

| June 30, 2006 (1) |

$ | 6.25 | $ | 5.90 | ||

| (1) | Represents the high and low bid information for our shares of units from June 15, 2006, the date that our Units first became separately tradable, through June 30, 2006. |

Common Stock

| Quarter ended |

High | Low | ||||

| December 31, 2007 |

$ | 5.84 | $ | 3.10 | ||

| September 30, 2007 |

$ | 5.86 | $ | 5.59 | ||

| June 30, 2007 |

$ | 5.86 | $ | 5.65 | ||

| March 30, 2007 |

$ | 5.67 | $ | 5.56 | ||

| December 31, 2006 |

$ | 5.59 | $ | 5.45 | ||

| September 30, 2006 |

$ | 5.50 | $ | 5.35 | ||

| June 30, 2006 (1) |

$ | 5.37 | $ | 5.35 | ||

| (1) | Represents the high and low bid information for our shares of common stock from June 15, 2006, the date that our common stock first became separately tradable, through June 30, 2006. |

Warrants

| Quarter ended |

High | Low | ||||

| December 31, 2007 |

$ | .495 | $ | .165 | ||

| September 30, 2007 |

$ | .355 | $ | .215 | ||

| June 30, 2007 |

$ | .395 | $ | .192 | ||

| March 30, 2007 |

$ | .34 | $ | .20 | ||

| December 31, 2006 |

$ | .32 | $ | .16 | ||

| September 30, 2006 |

$ | .31 | $ | .27 | ||

| June 30, 2006 (1) |

$ | .30 | $ | .28 | ||

| (1) | Represents the high and low bid information for our warrants from June 15, 2006, the date that our warrants first became separately tradable, through June 30, 2006. |

14

Holders of Common Equity

As of March 13, 2008, we had approximately 7 stockholders of record of our common stock. This does not include beneficial owners of our common stock, including Cede & Co., nominee of the Depository Trust Company.

Dividends

We have not paid any dividends on our common stock to date. The payment of dividends in the future will be contingent upon our revenues and earnings, if any, capital requirements and general financial condition. It is the present intention of our board of directors to retain all earnings, if any, for use in our business operations and, accordingly, our board of directors does not anticipate declaring any dividends in the foreseeable future. There are no restrictions on our ability to pay dividends.

Equity Compensation Plan Information

The following table provides information as of December 31, 2007 with respect to compensation plans (including individual compensation arrangements) under which our equity securities are authorized for issuance.

| Plan Category |

Number of securities to be issued upon exercise of outstanding options, warrants and rights |

Weighted-average exercise price of outstanding options, warrants and rights |

Number of securities remaining available for future issuance under equity compensation plans (excluding securities reflected in column (a)) | |||

| (a) | (b) | (c) | ||||

| Equity compensation plans approved by security holders |

None | Not Applicable | 2,000,000 | |||

| Equity compensation plans not approved by security holders |

Not Applicable | Not Applicable | Not Applicable | |||

| Total |

None | Not Applicable | 2,000,000 |

15

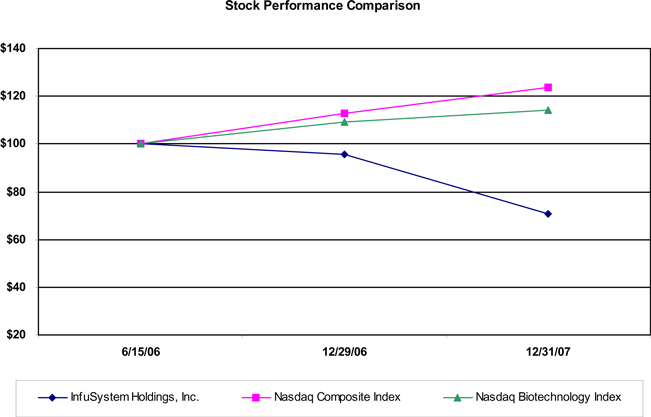

Stock Performance Graph

The graph set forth below compares the change in the our cumulative total stockholder return on our common stock between June 15, 2006, (the date that our common stock became separately tradeable from our units) and December 31, 2007 with the cumulative total return of the NASDAQ Composite Index and the NASDAQ Biotechnology Index during the same period. This graph assumes the investment of $100 on June 15, 2006 in our common stock and each of the comparison groups and assumes reinvestment of dividends, if any. We have not paid any dividends on our common stock, and no dividends are included in the report of our performance. This graph is not “soliciting material,” is not deemed filed with the SEC and is not to be incorporated by reference in of our filings under the Securities Act or the Exchange Act whether made before or after the date hereof and irrespective of any general incorporation language in any such filing.

| 6/15/06 | 12/29/06 | 12/31/07 | |||||||

| InfuSystem Holdings, Inc. Common Stock |

$ | 100 | $ | 95.56 | $ | 70.94 | |||

| Nasdaq Composite Index |

$ | 100 | $ | 112.65 | $ | 123.70 | |||

| Nasdaq Biotechnology Index |

$ | 100 | $ | 109.14 | $ | 114.14 | |||

16

Recent Sales of Unregistered Securities

As described in our Current Reports on Form 8-K filed on January 3, 2007, May 4, 2007 and September 12, 2007, during 2006 and 2007, we sold an aggregate of 1,357,717 warrants to purchase our common stock to members of our board of directors and our former Chief Financial Officer in private placement transactions made in reliance upon the exemption from securities registration afforded by Section 4(2) under the Securities Act and Regulation D thereunder.

Use of Proceeds from Registered Offering

On April 11, 2006, we commenced our initial public offering of 16,666,667 units, each consisting of one share of our common stock, par value $0.0001 per share, and two warrants, each exercisable for one share of our common stock, pursuant to a registration statement on Form S-1 (File No. 333-129035), which was declared effective on April 11, 2006. FTN Midwest Securities Corp. (“FTN Midwest”) served as underwriter for our initial public offering, which closed on April 18, 2006. The net proceeds from our initial public offering were $96,903,000, after deducting offering expenses of $497,000 and underwriting discounts of $2,600,000, including $1,000,000 evidencing the underwriters’ non-accountable expense allowance of 1% of the gross proceeds of the initial public offering. As of April 18, 2006, $95,000,000 of this amount had been placed in trust (including $5,400,000 payable to FTN Midwest for deferred underwriting discounts and commissions) for purposes of consummating a business combination, with $1,903,000 remaining.

On May 18, 2006, FTN Midwest exercised its over-allotment option in connection with our initial public offering and purchased 208,584 additional units. The net proceeds from the exercise of the over-allotment option were $1,232,000, after deducting underwriting discounts of $20,000. $1,215,000 of the net proceeds from the exercise of the over-allotment option was placed in trust (including $68,000 in deferred underwriters discounts and commissions) with $17,000 remaining.

As of December 31, 2006, we had expended all of the proceeds of our initial public offering held outside the trust account.

On October 25, 2007, we completed our acquisition of InfuSystem from I-Flow and disbursed the $101,257,000 balance in the trust account as set forth below.

| Description |

Amount | |||

| Payment to I-Flow in connection with closing of acquisition of InfuSystem |

$ | 73,829,000 | (1) | |

| Conversion of shares of common stock |

16,899,000 | (2) | ||

| Legal and other fees payable in connection with closing of acquisition of InfuSystem |

2,400,000 | (3) | ||

| Transferred to operating account |

8,129,000 | |||

| Total |

$ | 101,257,000 | ||

| (1) | Represents $67,297,000 cash portion of the $100,000,000 purchase price paid for InfuSystem plus an additional $6,532,000, which consisted of a $3,000,000 termination fee, financing fees of approximately $2,002,000, a ticking fee of $693,000 and other acquisition related reimbursements of approximately $837,000. The $32,703,000 remainder of the purchase price was paid in the form of a loan from I-Flow. |

| (2) | Represents cash consideration paid to stockholders who held 2,816,488 shares in the aggregate, and who voted against our acquisition of InfuSystem and elected to convert their shares of common stock into their pro rata portion of the proceeds of the trust account, or $6.00 per share. As a result of 90,000 less shares ultimately converted by stockholders voting against the acquisition, we received a refund of $6.00 per share or $540,000. |

| (3) | Includes payments of $200,000 to each of Sean McDevitt and Philip B. Harris pursuant to the Guarantee Fee and Reimbursement Agreement, dated as of September 29, 2006, by and among Sean McDevitt, Philip B. Harris, Pat LaVecchia and the Company in connection with their guaranty of the break up fee payable to I-Flow upon a termination of the Stock Purchase Agreement. |

17

On October 31, 2007, we paid a balance of $6,405,000 owed to FTN Midwest out of our operating account. The balance owed consisted of the items set forth below.

| Deferred underwriting fee |

$ | 4,555,000 | |

| M&A advisory fees and expenses |

1,850,000 |

As a result of 90,000 less shares ultimately converted by shareholders voting against our acquisition of InfuSystem, we paid an additional underwriting fee of $29,000 to FTN Midwest.

The remaining cash of approximately $2,200,000 has and will continue to be used for general corporate purposes.

Repurchases of Equity Securities

None.

| Item 6. | Selected Financial Data. |

InfuSystem Holdings, Inc. and Subsidiary

The following historical information was derived from the audited consolidated financial statements of InfuSystem Holdings, Inc. for the fiscal years ended December 31, 2007 and 2006 and for the period from August 15, 2005 (inception) to December 31, 2005 and the related notes and schedules thereto, which are included in this Annual Report on Form 10-K. The information for InfuSystem Holdings, Inc. for the fiscal year ended December 31, 2007 includes operations for InfuSystem from October 26, 2007 through December 31, 2007.

Statement of Operations Data (1)

| (in thousands, except per share data) | Year Ended December 31, 2007 |

Year Ended December 31, 2006 |

Period from August 15, 2005 (inception) to December 31, 2005 |

|||||||||

| Net revenues |

$ | 6,582 | $ | — | $ | — | ||||||

| Total operating expenses |

8,079 | 20,824 | 24 | |||||||||

| Total other (expense) income |

(189 | ) | 14,003 | (1 | ) | |||||||

| Income tax expense |

(1,110 | ) | (1,038 | ) | — | |||||||

| Net loss |

(2,796 | ) | (7,859 | ) | (25 | ) | ||||||

| Net loss per share – basic and diluted |

$ | (0.15 | ) | $ | (0.58 | ) | $ | (0.01 | ) | |||

| Balance Sheet Data (at period end) (1)

|

| |||||||||||

| (in thousands) | December 31, 2007 |

December 31, 2006 |

December 31, 2005 |

|||||||||

| Total assets |

$ | 116,426 | $ | 100,298 | $ | 177 | ||||||

| Long-term debt, including current maturities |

32,294 | — | — | |||||||||

| Stockholders’ equity |

68,759 | 65,146 | — | |||||||||

| (1) | On October 25, 2007, we completed our acquisition of 100% of the issued and outstanding capital stock of InfuSystem from I-Flow pursuant to the terms of the Stock Purchase Agreement. InfuSystem’s results of operations are included in our Consolidated Statements of Operations from the date of the acquisition. For more information, see Note 3 “Acquisitions” to our Consolidated Financial Statements which are included in this Annual Report on Form 10-K. |

18

Predecessor InfuSystem

The following historical information was derived from the audited financial statements of Predecessor InfuSystem for the period commencing after December 31, 2006 to October 25, 2007, the fiscal years ended December 31, 2006, 2005, 2004 and 2003 and the related notes and schedules thereto (“Predecessor InfuSystem”), which are included in this Annual Report on Form 10-K.

Statement of Operations Data

| January 1, 2007 to October 25, 2007 |

Year Ended December 31, 2006 |

Year Ended December 31, 2005 |

Year Ended December 31, 2004 |

Year Ended December 31, 2003 | |||||||||||

| Net revenues |

$ | 25,001 | $ | 31,716 | $ | 28,525 | $ | 19,349 | $ | 13,022 | |||||

| Cost of revenues |

6,702 | 8,455 | 7,735 | 5,555 | 3,993 | ||||||||||

| Total operating expenses |

15,673 | 15,091 | 12,709 | 9,142 | 7,130 | ||||||||||

| Income tax expense |

1,086 | 3,094 | 2,938 | 1,699 | 720 | ||||||||||

| Net income |

1,777 | 4,963 | 5,093 | 2,924 | 1,147 | ||||||||||

Balance Sheet Data (at period end)

| December 31, 2006 |

December 31, 2005 |

December 31, 2004 |

December 31, 2003 | |||||||||

| Total assets |

$ | 27,628 | $ | 27,831 | $ | 17,665 | $ | 11,647 | ||||

| Stockholders’ equity |

22,008 | 22,455 | 12,823 | 9,215 | ||||||||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operation. |

Executive Overview

Included in this Annual Report on Form 10-K are the results of operations of both the Company and Predecessor InfuSystem. The Company’s results of operations are presented for the fiscal years ended December 31, 2007 and 2006 and for the period from August 15, 2005 (inception) to December 31, 2005. The Company’s results of operations for the fiscal year ended December 31, 2007 include the operations of InfuSystem for a sixty seven day period from October 26, 2007 to December 31, 2007. The results of operations of Predecessor InfuSystem are presented for the fiscal years ended December 31, 2006 and 2005 and for the period commencing after the end of the fiscal year ended December 31, 2006 to October 25, 2007, the date of consummation of the acquisition. Also included in this Annual Report on Form 10-K is a discussion and analysis of the Company’s management with respect to Predecessor InfuSystem’s fiscal years ended December 31, 2006 and 2005 and for the period commencing after the end of the fiscal year ended December 31, 2006 to October 25, 2007, the date of consummation of the acquisition. Management’s Discussion and Analysis has been prepared by the Company based upon its understanding of and in reliance upon information communicated to the Company by former InfuSystem management regarding the reasons for the changes in Predecessor InfuSystem’s operations.

The financial statements and supplementary data of Predecessor InfuSystem presented for the period prior to October 26, 2007 are not those of the Company and were prepared by the former management of Predecessor InfuSystem and audited by Predecessor InfuSystem’s independent registered public accounting firm. The financial statements and supplementary data of Predecessor InfuSystem for the period prior to October 26, 2007 may be particularly unrepresentative of the operations of the Company going forward for the following reasons, among others:

| • | Both the Company’s financials and Predecessor InfuSystem’s financials contain items which require management to make considerable judgments and estimates. There can be no assurance that the judgments and estimates made by the Company’s management will be identical or even similar to the historical judgments and estimates made by Predecessor InfuSystem’s former management. |

19

| • | The financials of Predecessor InfuSystem contain allocations of certain general and administrative expenses specific to I-Flow. |

| • | The Company’s financials are prepared utilizing a different basis of accounting than Predecessor InfuSystem’s financials. Specific differences include, but are not limited to, the Company’s accounting for net property, intangible assets and goodwill at fair value on the date of acquisition in accordance with SFAS No. 141, Business Combinations. Predecessor InfuSystem accounted for these items on a historical cost basis. |

InfuSystem Holdings, Inc. Overview

We were formed as a Delaware blank check company in 2005 for the purpose of acquiring through a merger, capital stock exchange, asset acquisition or other similar business combination, one or more operating businesses in the healthcare sector. On September 29, 2006, we entered into a Stock Purchase Agreement with I-Flow, Iceland Acquisition Subsidiary and InfuSystem. Upon the closing of the transactions contemplated by the Stock Purchase Agreement on October 25, 2007, Iceland Acquisition Subsidiary purchased all of the issued and outstanding capital stock of InfuSystem from I-Flow and concurrently merged with and into InfuSystem. As a result of the merger, Iceland Acquisition Subsidiary ceased to exist as in independent entity and InfuSystem, as the corporation surviving the merger, became our wholly-owned subsidiary. Effective October 25, 2007, we changed our corporate name from “HAPC, INC.” to InfuSystem Holdings, Inc. Upon our acquisition of InfuSystem, we ceased to be a development stage company and became an operating company.

Summary of Revenue and Expenses

The following table provides a summary of our revenues and expenses for the fiscal years ended December 31, 2007, 2006 and 2005 to supplement the more detailed discussions below:

| Years ended December 31, | ||||||||||||

| (in thousands) |

2007 | 2006 | 2005 | |||||||||

| Net revenues |

$ | 6,582 | $ | — | $ | — | ||||||

| Cost of revenues |

||||||||||||

| Product and supply costs |

$ | (923 | ) | $ | — | $ | — | |||||

| Pump depreciation |

(697 | ) | — | — | ||||||||

| Total cost of revenues |

$ | (1,620 | ) | $ | — | $ | — | |||||

| Provision for doubtful accounts |

$ | (584 | ) | $ | — | $ | — | |||||

| Amortization of intangibles |

$ | (335 | ) | $ | — | $ | — | |||||

| Selling and marketing expenses |

||||||||||||

| Sales salaries, commissions, fringes and payroll-related |

$ | (524 | ) | $ | — | $ | — | |||||

| Travel and entertainment |

(88 | ) | — | — | ||||||||

| Marketing |

(27 | ) | — | — | ||||||||

| Other |

(10 | ) | — | — | ||||||||

| Total selling and marketing expenses |

$ | (649 | ) | $ | — | $ | — | |||||

| General and administrative expenses |

||||||||||||

| Share-based compensation expense |

$ | (1,750 | ) | $ | (19,710 | ) | $ | (24 | ) | |||

| Admin. salaries, fringes and payroll-related |

(1,168 | ) | — | — | ||||||||

| Ticking fee |

(630 | ) | (95 | ) | ||||||||

| Insurance |

(307 | ) | — | — | ||||||||

| Other |

(1,036 | ) | (1,019 | ) | — | |||||||

| Total general and administrative expenses |

$ | (4,891 | ) | $ | (20,824 | ) | $ | (24 | ) | |||

| (Loss) gain on derivatives |

||||||||||||

| (Loss) gain on warrants |

$ | (3,037 | ) | $ | 10,800 | $ | — | |||||

| Loss on interest rate swap |

(257 | ) | — | — | ||||||||

| Total (loss) gain on derivatives |

$ | (3,294 | ) | $ | 10,800 | $ | — | |||||

| Interest income |

$ | 3,879 | $ | 3,204 | $ | — | ||||||

| Interest expense |

||||||||||||

| Interest on term loan |

$ | (637 | ) | $ | — | $ | — | |||||

| Amortization of deferred debt issuance costs |

(134 | ) | — | — | ||||||||

| Swap income |

4 | — | — | |||||||||

| Other |

(7 | ) | (1 | ) | (1 | ) | ||||||

| Total interest expense |

$ | (774 | ) | $ | (1 | ) | $ | (1 | ) | |||

| Income tax expense |

$ | (1,110 | ) | $ | (1,038 | ) | $ | — | ||||

20

InfuSystem Holdings, Inc. Results of Operations for the Fiscal Year ended December 31, 2007

Our results of operations for the year ended December 31, 2007 are not comparable with the prior periods presented. Effective October 25, 2007, upon our acquisition of InfuSystem, we ceased to be a development stage company and became an operating company. Substantially all activity through October 25, 2007 relates to our formation, initial public offering (the “IPO”) and efforts related to the acquisition of InfuSystem.

Our revenue consists predominantly of rental revenue derived from our rental of ambulatory infusion pumps which are primarily used for continuous infusion of chemotherapy drugs for patients with colorectal cancer. Our revenue for the fiscal year ended December 31, 2007 was $6,582,000, which includes InfuSystem revenue only for the sixty seven day period from October 26, 2007 to December 31, 2007. Management anticipates that new revenue growth will come from the expansion of the existing use of our ambulatory infusion pumps for the treatment of colorectal cancer as well as the potential future use of our ambulatory infusion pumps for continuous infusion of chemotherapy drugs for the treatment of head, neck and gastric cancer. Another aspect of our business strategy over the next one to three years is to actively pursue opportunities for the expansion of our business through acquisitions, joint ventures and strategic alliances.

Cost of revenues for the fiscal year ended December 31, 2007 was $1,620,000. This consisted of product and supply costs, including freight costs for the transport of pumps and supplies to and from oncology practices, and depreciation on our infusion pumps.

Provision for doubtful accounts for the fiscal year ended December 31, 2007 was $584,000.

21

Amortization of our intangible assets for the fiscal year ended December 31, 2007 was $335,000.

During the fiscal year ended December 31, 2007, our selling and marketing expenses were $649,000. Selling and marketing expenses during this period consisted of sales salaries, commissions and associated fringe benefit and payroll-related items, travel and entertainment, marketing and other miscellaneous expenses.

During the fiscal year ended December 31, 2007, our general and administrative expenses were $4,891,000. General and administrative expenses during this period consist primarily of share-based compensation expense, administrative personnel (including management and officers) salaries, fringes and payroll-related items, the ticking fee we paid to I-Flow on the date of the acquisition of InfuSystem, insurance (including directors’ and officers’ insurance) and other miscellaneous expenses.

During the fiscal year ended December 31, 2007, we recorded a loss on derivatives of $3,294,000. This amount represents an unrealized loss which resulted from the change in the fair value of our warrants and the change in the fair value of our single interest rate swap. For more information, please refer to the discussion under “Summary of Significant Accounting Policies—Warrants and Derivative Financial Instruments” included in Note 2 and “Warrants and Derivative Financial Instruments” included in Note 7 to our Consolidated Financial Statements included in this Annual Report on Form 10-K.

During the fiscal year ended December 31, 2007, we recorded interest income of $3,879,000. This amount consists primarily of interest earned on the trust account (in which a substantial portion of the proceeds of our initial public offering were deposited) through the date of the acquisition. Interest income is not expected to be significant going forward.

During the fiscal year ended December 31, 2007, we recorded interest expense of $774,000. This amount consists of interest paid to I-Flow on our term loan, the amortization of deferred debt issuance costs incurred in conjunction with the loan, income on the interest rate swap and other interest expense.

During the fiscal year ended December 31, 2007, we recorded income tax expense of $1,110,000. This amount consists of federal, state and local tax provisions.

Management believes that there has been no material effect on our operations or financial condition as a result of inflation or changing prices of our ambulatory infusion pumps during the period from August 15, 2005 (inception) through December 31, 2007.

InfuSystem Holdings, Inc. Results of Operations for the Fiscal Year ended December 31, 2006