Morgan, Lewis & Bockius LLP

101 Park Avenue

New York, NY 10178

March 24, 2006

VIA EDGAR

Securities and Exchange Commission

450 Fifth Street, N.W.

Washington, D.C. 20549

| Re: | Healthcare Acquisition Partners Corp. – Amendment No. 4 to Registration Statement on Form S-1 |

Ladies/Gentlemen:

We are transmitting for filing Amendment No. 4 to the Registration Statement on Form S-1 (the “Registration Statement”) of Healthcare Acquisition Partners Corp.

The Registration Statement was initially filed on October 14, 2005, Amendment No. 1 to the Registration Statement was filed on December 8, 2005, Amendment No. 2 to the Registration Statement was filed on January 17, 2006 and Amendment No. 3 to the Registration Statement was filed on March 3, 2006. The Amendment No. 4 to the Registration Statement being filed today responds to comments of the Staff contained in a letter dated March 21, 2006. A memorandum containing Healthcare Acquisition Partners Corp.’s specific responses to the Staff’s comments is attached.

Please direct any questions regarding the attached filing to the undersigned at 212-309-6127, or to Howard Kenny at 212-309-6843.

Thank you.

Very truly yours,

/s/ Christopher O. Hathaway

Christopher O. Hathaway

| cc: | Healthcare Acquisition Partners Corp. |

FTN Midwest Securities Corp.

Jack Kantrowitz, Esq.

Summary

| 1. | We note the disclosure that the Warrant Purchase Agreement may be effected by affiliates or designees of one or more of the Management Members. Please disclose the purpose for purchases by affiliates or designees and disclose whether any of the warrants purchased pursuant to the Warrant Purchase Agreement will be subject to any restrictions on transfer after purchase. Additionally, disclose whether it is possible that any affiliates of the Broker effecting such purchases may locate a target for the company. |

Response: The terms by which members of management will effect the warrant purchases have been changed. These purchases will be effected by the management members only and not by their “affiliates or designees”. In addition, member of management will agree that any warrants purchased may not be transferred until the Company completes its initial business combination. The prospectus has been revised in the summary and throughout the prospectus to reflect the foregoing.

Additionally, it is not the intent of the Company to engage affiliates of the broker dealer effecting the warrant purchases to locate an acquisition candidate. This prospectus has been revised to disclose the foregoing.

| 2. | We note your disclosure on page 3 that the common stock held by the your stockholders, and any additional shares issued from the reserved treasury shares, will be subject to lock-up agreements restricting the sale or other transfer until six months after your initial business combination is completed. However, it appears from the form of agreement attached as Exhibit 10.6 that such restrictions on transfer do go into effect until the consummation of a business combination. Please reconcile that advise. Additionally, please disclose the reasons for allowing such transfer upon the consent of the company and the underwriter. We may have further comment. |

Response: The lock-up period commences upon the pricing of the offering and continues until the date that is six months after the initial business combination is completed. The form of agreement attached as Exhibit 10.6 has been revised to clarify this.

The lock-up agreements require the consent of both the underwriter and the Company (unlike the more typical lock-up which can be waived by the underwriter alone) because each has an interest in maintaining it. The underwriter wants to be able to control trading in the period right after the IPO to help an orderly market develop; both the Company and the underwriter have determined that it is in the interest of public purchasers of the units for the insiders not to be able to trade prior to the completion of the business combination (plus 6 months).

| 3. | We note your response to comment 1 from our letter of February 8, 2006, However, it still appears that Paragraphs A and B to Article Fifth of your Amended and Restated Articles of Incorporation would require you to provide for 19.9 percent conversion in connection with every business combination structured. |

Paragraph A of Section FIFTH states that “In the event that a majority of the IPO Shares…case at the meeting to approve the Business Combination are voted for the approval of such Business Combination, the corporation shall be authorized to consummate the Business Combination; provided, that the corporation shall not

consummate a Business Combination if holders representing 20% or more in interest of the IPO Shares exercise their conversion rights described in paragraph B below.” It therefore appears to provide for a two prong approval process from the IPO shareholders: greater than 50% approving the transaction and less than 20% electing conversion.

Paragraph B provides that conversion must be elected at the same time that a shareholder votes against a business combination, and that “In the event that a Business Combination is approved in accordance with paragraph A above…any stockholder of the corporation holding shares of Common Stock issued by the corporation in its initial public offering…of securities who voted against the Business Combination may, contemporaneous with such vote, demand that the corporation convert his, her or its IPO Shares into cash. If so demanded, the corporation shall convert such shares at a per share conversion price equal to…”

In light of Paragraph B’s mandate that “the corporation shall convert such shares” for any IPO shareholder who demanding conversion, and the absence of any specific exceptions to the general rule of 20% conversion in Paragraph A, it appears that Article Fifth would require the company to provide for 19.99 percent conversion in connection with every business combination structured. Please advise or revise.

Response: The prospectus has been revised to remove the statements that the business combination may be conditioned upon the non-exercise of conversion rights by a percentage of stockholders lower than 20%. In addition, a statement has been added to the effect that the Company will effect a business combination in accordance with its terms if (a) the majority vote is obtained and (b) less than 20% of the public stockholders exercise their conversion rights.

| 4. | We note your supplemental response to comment two from our letter of February 8, 2006 that the shares issued to management were not for cash consideration but rather were issued in consideration of such individuals accepting their positions with the company. Please revise the disclosure on page 2 to clearly state this. Also, discuss the consideration to be provided for the 2,416,666 shares reserved as treasury stock. |

Response: The prospectus has been revised on page 2 and elsewhere to clearly state that the shares issued to management were issued for no cash consideration. In addition, the prospectus has been revised to state that the consideration to be provided for treasury shares that may be issued, if any, will be determined by the Board of Directors at the time of any such issuance.

Risk Factors, page 10

| 5. | We note your disclosure that, though the company and its board of directors have “no intention of doing so, Delaware law may allow [you] to amend” Article FIFTH of your Amended and Restated Certificate of Incorporation, relating to certain requirements and restrictions relating to this offering. Please revise your document throughout in order to provide a thorough discussion of the consequences of any such revisions to each of the company, the board of directors and the stockholders, including but not limited to the financial, economic and legal consequences on each group. Alternatively, clarify the |

disclosure to indicate that such provisions will not be revised or amended. We may have further comment.

Response: The prospectus has been revised to indicate that the Board of Directors of the Company will not propose to the stockholders that the provisions contained in Article Fifth of the Amended and Restated Certificate of Incorporation be revised or amended.

Certain Relationships and Related Transactions, page 50

| 6. | We note that you name only Mr. McDevitt as a promoter of the company. It appears that each of your officers and directors is a promoter. Please revise or advise why any or all of them are not. |

Response: The prospectus has been revised on page 50 to list each of the Company’s officers and directors as a promoter.

Management Warrant Purchase, page 52

| 7. | We note exhibit 10.11 includes the circumstances where Sean McDevitt and Pat LaVecchia will not purchase warrants. Please include disclosure in this section. |

Response: The “Management Warrant Purchase” section on page 52 has been revised to include disclosure regarding the circumstances under which Messrs. McDevitt and LaVecchia will not purchase warrants.

Underwriting, page 62

| 8. | We note the removal of the paragraph following the table relating to the affiliation between Healthcare Acquisition Partners and FTN Midwest Securities Corp. Please add back this disclosure or explain why such disclosure is no longer required. We may have further comment. |

Response: The section of “Underwriting” discussing the affiliation of the Company and FTN Midwest Securities Corp., and the engagement of a qualified independent underwriter (“QIU”) to assist in the pricing has been removed. The Company has repurchased all shares previously held by FTN Midwest and under the terms of the revised agreements between the underwriter and the Company, the underwriter and its affiliated parties will not hold 10% or more of the equity of the Company; as a result, there is no affiliation as of the date hereof. FTN Midwest has confirmed with the NASD that no QIU is required in these circumstances.

Notes to financial statements

Note 1 – Organization, business operations and significant accounting policies, F-7

| 9. | Please revise to include your accounting policy for stock based compensation and include the disclosure required by APB 25, SFAS 123, and SFAS 148 as appropriate. |

Response: The Company has revised the financial statements to address the Staff’s comments as stated above, as follows:

The Company applies APB Opinion No. 25 (Accounting for Stock Issued to Employees) and related Interpretations in accounting for stock based compensation. Accordingly, compensation for shares issued to officers and directors is measured using their intrinsic value at the date of the opportunity to acquire such shares and recognized as compensation expense ratably over the vesting period.

Note 5 – Common and preferred stock, F-10

| 10. | We note your response to our prior comment 5 (and your reference to the response to comment 2); however we do not see where you have addressed our comment in its entirety. Therefore, we are reissuing our comment in part. Describe how your determination of the value of the shares issued as compensation (i.e. $10,500 for 1,750,001 shares on December 30, 2005) complies with GAAP. Since there was a firm commitment, it would appear the fair value of the stock would be more readily determinable that the fair value of the services to be performed. Tell us how you determined $.006 per share represented fair value, considering the $6 per unit commitment price (as disclosed in your initial S-1 on October 15, 2005) prior to the issuance of the shares. Your response should include objective evidence supporting your determination for the fair value of shares issued and compensation cost recorded. Refer to the authoritative literature noted in the comment above. |

Response: Staff Accounting Bulletin Topic 4D requires that stock-based compensation be determined in accordance with generally accepted accounting principles (GAAP). The Company has applied APB No. 25, which “requires compensation cost for stock-based employee compensation plans to be recognized based on the difference if any, between the quoted market price of the stock and the amount an employee must pay to acquire the stock.”

In this case, the shares were issued to directors and officers for no cash consideration. At the time the shares were issued, there was no quoted market price. Therefore, the Company has recognized a compensation expense equal to the estimated fair value of the shares at the time of issuance. The shares were issued to directors and officers pursuant to arrangements entered into in September and October 2005; certificates were issued on December 30, 2005. The Company believes there is no difference between the fair value of the shares between September 2005 and December 2005.

The Company has recognized compensation expense based on a per share value of $0.22. The Company has determined this value as follows.

The proposed initial public offering price of the units being registered is $6.00 per unit. The units offered to the public are different in several significant respects from the shares granted to management. The units include both shares and warrants while the shares issued to the directors and officers have no accompanying warrants. Only the shares included in the publicly registered units will have a claim to the trust proceeds. The units and the shares and warrants they include are immediately tradable. Nevertheless, the Company has used the $6.00 IPO price for the units as a starting point for determining the fair value of the shares granted to directors and officers in 2005.

The table below reconciles the Company’s value of $0.22 per share to the $6.00 per unit IPO price.

| Healthcare Acquisition Partners Corp Share value analysis |

| |||

| IPO price per unit |

$ | 6.00 | ||

| Trading discount |

$ | (0.62 | ) | |

| Dilution discount |

$ | (1.39 | ) | |

| Lock-up discount |

$ | (1.80 | ) | |

| Net value |

$ | 2.19 | ||

| Expected value discount |

$ | (1.97 | ) | |

| Value per share @ time of transfer |

$ | 0.22 | ||

The “trading discount” refers to the expected trading value of a standalone share of common stock after the IPO is completed. Viewed another way, the discount subtracts the value of the warrants which begin trading separately from the common stock after the IPO. As indicated in Exhibit A hereto, standalone shares of common stock in SPACs have tended to trade very near the per share trust amount. In December 2005 when shares were issued to management, the Company intended to put IPO proceeds into trust in an amount equal to $5.38 per share. For this reason, the Company has applied a $0.62 discount.

The “dilution discount” refers to the dilution that will occur upon exercise of the warrants included in the units to be offered to the public. The calculation of this $1.39 discount is set forth in Exhibit B.

The “lockup discount” refers to the fact that the shares issued to the directors and officers are subject to vesting requirements and may not be traded until six months after the consummation of the initial business combination. It is typical for insider shares to be locked up for 180 days after an IPO. The Company has applied a discount of 10% for each period of six months beyond this typical lockup period (assuming a business combination is completed in 24 months), resulting in a discount of $1.80.

As a result of the foregoing discounts, the net value of the share equals $2.19.

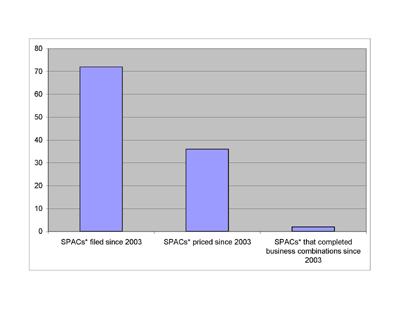

As further explained in Exhibit C, the “expected value” discount reflects the fact that the Company has further discounted the share value to account for the fact that at the time the shares were issued to management there was no assurance that either the initial public offering or a business combination would be completed within the timeframe set forth in the prospectus. To the extent that either of those events do not occur, the shares issued to the directors and officers are completely worthless. The Company has analyzed the probability of these events occurring based on the history of other SPACs at approximately the time when the shares were issued to the directors and officers. Based on publicly available information in December 2005, only 2.8% of all SPACs that had filed S-1s had successfully completed a business combination. To be conservative, the Company has used a probability of 10%, rather than 2.8%, and has, therefore, further discounted the value of the shares granted to management from $2.19 to $0.22.

| 11. | We noted that you recorded $10,500 compensation expense for the entire issuance of shares to certain members of the management team. We also noted that shares issued may be forfeited if termination of services occurs prior to certain future dates (i.e. vesting period). Considering the vesting period and forfeit provisions, tell us how you determined it was appropriate to record the entire compensation cost in the period ended December 31, 2005 and why no unearned compensation (reduction to equity) was recorded. Refer to paragraphs (11a) and (14) of APB 25. |

Response: As stated in paragraph 11(a) of APB 25, even though shares issued may be forfeited if termination of services occurs prior to vesting, measuring compensation using the cost to an employer corporation of reacquired stock distributed through a stock option, purchase, or award plan is not acceptable practice. Therefore, the Company has determined that the fair value of the shares issued to management, computed using their intrinsic value at the date of the opportunity to acquire such shares, was $0.22 per share, resulting in a compensation charge of $385,000. The Company is recognizing this charge over the 24 month vesting period, as required by paragraph 14 of APB 25, and has revised its financial statements to include unearned stock compensation as a reduction to its equity.

| Historical SPAC Trading Discount | Exhibit A |

Trading price per share vs. amount held in trust per share for single unit SPACs that have priced since 2003 and that have not yet completed an acquisition

| Issuer Name |

IPO date |

Initial unit price |

12/27/05 market price |

Amount held in trust per share |

Market price as % of amount held in trust |

# days since IPO | ||||||||||

| Boulder Specialty Brands |

16-Dec-05 | $ | 8.00 | (a | ) | $ | 7.71 | NA | 12 | |||||||

| Star Maritime Acquisition |

16-Dec-05 | 10.00 | (a | ) | 9.66 | NA | 12 | |||||||||

| Endeavor Acquisition |

15-Dec-05 | 8.00 | (a | ) | 7.48 | NA | 13 | |||||||||

| Cold Spring Capital Inc |

10-Nov-05 | 6.00 | 5.21 | 5.49 | 95 | % | 48 | |||||||||

| Platinum Energy Resources Inc |

25-Oct-05 | 8.00 | 6.90 | 7.32 | 94 | % | 64 | |||||||||

| Paramount Acquisitions Corp |

24-Oct-05 | 6.00 | (a | ) | 5.30 | NA | 65 | |||||||||

| Key Hospitality Acquisition Corp |

24-Oct-05 | 8.00 | (a | ) | 7.25 | NA | 65 | |||||||||

| Federal Services Acquisition Corp |

19-Oct-05 | 6.00 | 5.32 | 5.58 | 95 | % | 70 | |||||||||

| Coconut Palm Acquisition Corp |

9-Sep-05 | 6.00 | 5.22 | 5.43 | 96 | % | 110 | |||||||||

| Ad.Venture Partners Inc |

26-Aug-05 | 6.00 | 5.33 | 5.60 | 95 | % | 124 | |||||||||

| Ithaka Acquisition Corp |

17-Aug-05 | 6.00 | 5.10 | 5.30 | 96 | % | 133 | |||||||||

| Stone Arcade Acquisition Corp |

16-Aug-05 | 6.00 | 5.32 | 5.54 | 96 | % | 134 | |||||||||

| Chardan North China Acquisition Corp |

5-Aug-05 | 6.00 | 5.70 | 5.17 | 110 | % | 145 | |||||||||

| Chardan South China Acquisition Corp |

5-Aug-05 | 6.00 | 5.62 | 5.17 | 109 | % | 145 | |||||||||

| Healthcare Acquisition Corp |

29-Jul-05 | 8.00 | 7.07 | 7.22 | 98 | % | 152 | |||||||||

| Oakmont Acquisition Corp |

18-Jul-05 | 6.00 | 5.23 | 5.39 | 97 | % | 163 | |||||||||

| Fortress America Acquisition Corp |

15-Jul-05 | 6.00 | 5.22 | 5.38 | 97 | % | 166 | |||||||||

| Israel Technology Acquisition Corp |

14-Jul-05 | 6.00 | 5.08 | 5.20 | 98 | % | 167 | |||||||||

| Courtside Acquisition Corp |

30-Jun-05 | 6.00 | 5.15 | 5.31 | 97 | % | 181 | |||||||||

| Services Acquisition Corp International |

30-Jun-05 | 8.00 | 7.13 | 7.32 | 97 | % | 181 | |||||||||

| Tac Acquisition Corp |

28-Jun-05 | 6.00 | 5.39 | 5.50 | 98 | % | 183 | |||||||||

| KBL Healthcare Acquisition Corp II |

21-Apr-05 | 6.00 | 5.25 | 5.30 | 99 | % | 251 | |||||||||

| Terra Nova Acquisition Corp |

19-Apr-05 | 6.00 | 5.08 | 5.17 | 98 | % | 253 | |||||||||

| Ardent Acquisition Corp |

24-Mar-05 | 6.00 | 5.23 | 5.20 | 101 | % | 279 | |||||||||

| Aldabra Acquisition Corp |

24-Feb-05 | 6.00 | 5.32 | 5.33 | 100 | % | 307 | |||||||||

| Coastal Bancshares Acquisition Corp |

18-Feb-05 | 6.00 | 5.11 | 5.16 | 99 | % | 313 | |||||||||

| Millstream II Acquisition Corp |

15-Feb-05 | 6.00 | 5.27 | 5.16 | 102 | % | 316 | |||||||||

| China Unistone Acquisition Corp |

13-Dec-04 | 6.00 | 6.43 | 5.10 | 126 | % | 380 | |||||||||

| Rand Acquisition Corp UTS |

18-Nov-04 | 6.00 | 5.39 | 5.16 | 104 | % | 405 | |||||||||

| Sand Hill IT Security Acquisition Corp |

27-Oct-04 | 6.00 | 5.19 | 5.10 | 102 | % | 427 | |||||||||

| Arpeggio Acquisition Corp Unit |

25-Aug-04 | 6.00 | 5.33 | 5.14 | 104 | % | 490 | |||||||||

| Tremisis Energy Acquisition Corp UTS |

30-Jul-04 | 6.00 | 5.52 | 5.18 | 107 | % | 516 | |||||||||

| Great Wall Acquisitions Corp |

29-Jul-04 | 6.00 | 5.23 | 5.10 | 103 | % | 517 | |||||||||

| CEA Acquisition Corp |

13-Feb-04 | 6.00 | 5.48 | 5.10 | 107 | % | 684 | |||||||||

| (a) | SPACs where shares & warrants have not yet begun trading separately |

| Mean |

101% | |

| Median |

98% |

| HAPC Trading Discount Calculation | ||||

| IPO value per unit |

$ | 6.00 | ||

| Amount held in trust per share |

$ | 5.38 | ||

| Share trading discount from IPO unit price |

$ | (0.62 | ) |

Exhibit B

Healthcare Acquisition Partners Corp

Dilution Discount Analysis

Original Cap Table

| Shares |

% (w/o warrants) |

||||

| Initial D&O shares |

1,750,001 | 9.5 | % | ||

| New investors |

16,666,667 | 90.5 | % | ||

| Total units |

18,416,668 | 100.0 | % | ||

| Warrants |

33,333,334 | n/a | |||

| Total shares & warrants |

51,750,002 | n/a | |||

Cap Table w/ Dilution (exercise of warrants)

| Shares |

% (w/o warrants) |

||||||||

| Initial D&O shares |

1,750,001 | 7.3 | % | ||||||

| New investors |

16,666,667 | 69.5 | % | ||||||

| New warrants |

33,333,334 | 139.0 | % | new warrants exercised @ $5.00 per share | |||||

| Treasury stock |

(27,777,778 | ) | -115.9 | % | treasury stock method; assumed buyback of shares w/warrant proceeds @ $6.00 per share | ||||

| 22,222,223 | 92.7 | % | |||||||

| Total shares |

23,972,224 | 100.0 | % | ||||||

| Fully diluted value of initial shares |

$ | 4.61 | fully diluted share basis utilizing treasury stock method | ||||||

| IPO unit price |

$ | 6.00 | |||||||

| Dilution discount |

$ | (1.39 | ) | represents 23% dilution | |||||

7

| SPAC historical success rates of business combinations | Exhibit C |

| SPACs* filed since 2003 |

72 | ||

| SPACs* priced since 2003 |

36 | ||

| SPACs* that completed business combinations since 2003 |

2 | ||

| Historical probability of business combination for filed SPAC |

2.8 | % | |

| Historical probability of business combination for priced SPAC |

5.6 | % | |

| * Single Unit SPACs |

| Expected value calculation | ||||||

| Net value per share (after trading, dilution & lock-up discount) |

$ | 2.19 | ||||

| Estimated probability of successful business combination |

10 | % | (Actual percentage of successful business combinations is much lower) | |||

| Value per share if no business combination |

$ | — | ||||

| Expected value |

$ | 0.22 | =($2.19 x 10%) + ($0.00 x 90%) | |||

| Discount for expected value |

$ | (1.97 | ) |